- If you are wondering whether Block is attractively priced after a volatile few years or if the current share price already reflects its potential, this breakdown is intended to help you frame that value question clearly.

- Block recently closed at US$59.97, with the share price showing a 0.3% decline over 7 days, a 9.6% decline over 30 days, an 8.0% decline year to date, a 22.2% gain over the past year, and a 78.1% decline over 5 years.

- Recent coverage has focused on Block's position in diversified financial services and how its business model fits into ongoing shifts in digital payments and financial technology. This backdrop has helped shape how investors interpret the recent mix of shorter term weakness and longer term performance.

- Simply Wall St's valuation model currently gives Block a valuation score of 3 out of 6. The sections that follow compare different valuation approaches and also point to a potentially more useful way to think about what the market might be missing by the end of the article.

Approach 1: Block Excess Returns Analysis

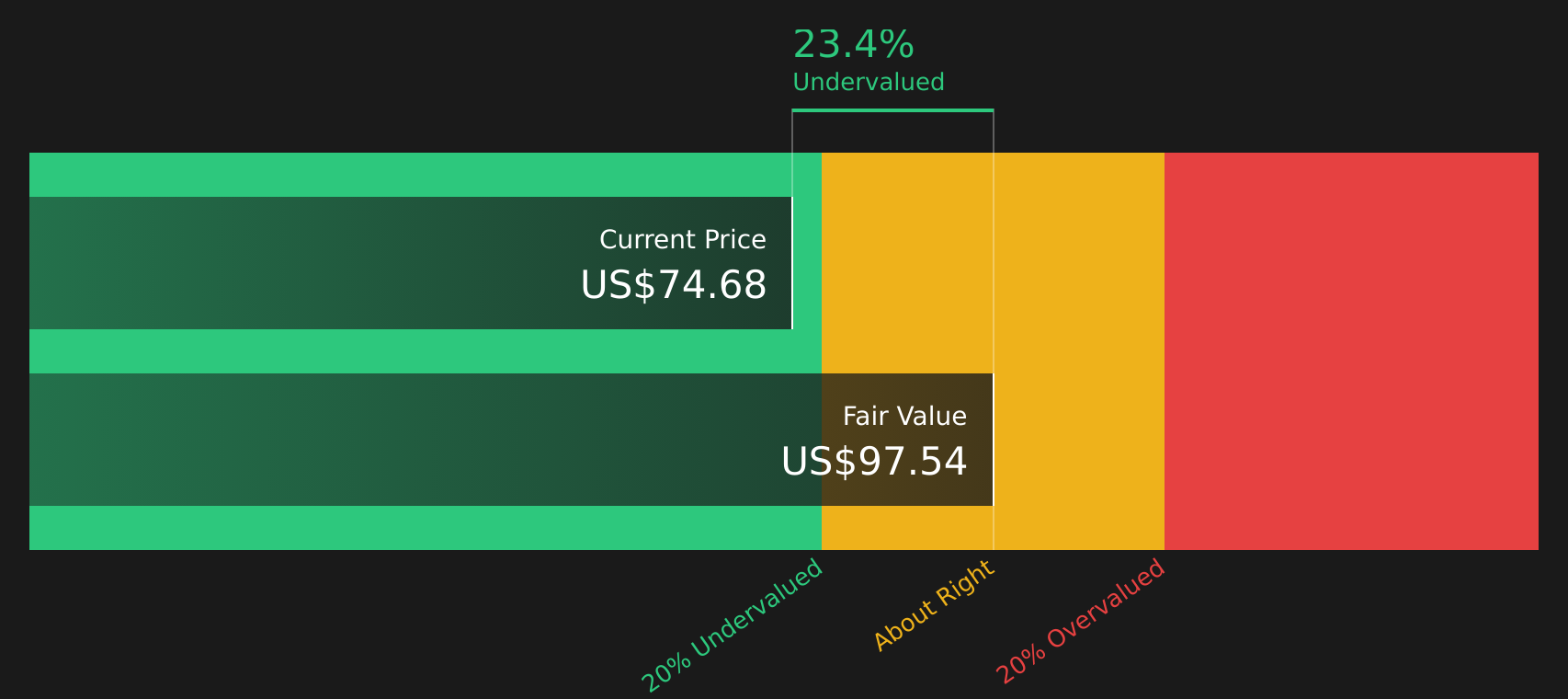

The Excess Returns model looks at how much profit a company is expected to generate above the return that equity investors require, based on its book value and profitability. Instead of focusing on cash flows, it concentrates on how efficiently each dollar of equity is used over time.

For Block, the model uses a Book Value of $36.88 per share and a Stable EPS estimate of $5.30 per share, sourced from weighted future Return on Equity estimates from 8 analysts. The Average Return on Equity is 11.38%. The Cost of Equity is $3.56 per share, which implies an Excess Return of $1.75 per share. A Stable Book Value of $46.59 per share, based on estimates from 7 analysts, is used to extend these economics into the future.

Feeding these inputs into the Excess Returns framework produces an estimated intrinsic value of about $87.93 per share. Compared with the recent share price of US$59.97, the model output suggests the stock is 31.8% undervalued according to this approach.

Result: UNDERVALUED

Our Excess Returns analysis suggests Block is undervalued by 31.8%. Track this in your watchlist or portfolio, or discover 61 more high quality undervalued stocks.

Approach 2: Block Price vs Earnings

For profitable companies, the P/E ratio is a useful shorthand because it links what you pay directly to the earnings the business is currently generating. Investors usually accept a higher P/E if they expect stronger growth or see lower risk in those earnings, while slower growth or higher risk tends to justify a lower, more cautious multiple.

Block currently trades on a P/E of 27.41x. That sits above the Diversified Financial industry average of 15.99x and also above the peer group average of 24.37x. Simply Wall St’s Fair Ratio metric for Block is 21.72x. This Fair Ratio is designed to be more tailored than a simple comparison with peers or the broad industry because it incorporates factors such as earnings growth expectations, profit margins, company size and identified risks into a single reference multiple.

When the actual P/E of 27.41x is set against the Fair Ratio of 21.72x, the market price implies a richer earnings multiple than the level suggested by these fundamentals. This points to Block looking overvalued on this metric alone.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Upgrade Your Decision Making: Choose your Block Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives give you a simple way to connect your view of Block’s story to the numbers by letting you pair your own assumptions for future revenue, earnings and margins with a Fair Value, compare that Fair Value with the current price to decide whether the stock looks attractive or stretched, see that view update automatically when fresh news or earnings arrive, and explore how other investors on Simply Wall St’s Community page can look at the same company very differently. For example, one Narrative on Block is currently using a Fair Value of about US$57.13 and another is using about US$111.06.

For Block however we'll make it really easy for you with previews of two leading Block Narratives:

These sit on opposite sides of the fence, so you can see how different assumptions about growth, margins and risk translate into very different fair values.

Fair value: US$85.52

Implied undervaluation vs last close: about 29.9%

Revenue growth assumption: 10.77%

- Expects AI driven efficiency, product velocity and workforce changes to support higher long term profitability and revenue.

- Assumes continued traction from Cash App, embedded banking, lending and cryptocurrency features, as well as international expansion.

- Aligns closely with the current analyst consensus target, with the view that the market is pricing Block below this fair value estimate.

Fair value: US$57.13

Implied overvaluation vs last close: about 5.0%

Revenue growth assumption: 9.87%

- Builds in heavier impact from regulatory requirements, cyber risk and reliance on cryptocurrency related revenue.

- Assumes tougher competition and pressure from government backed payment systems that could limit revenue growth and compress margins.

- Uses a lower fair value than the current price, with more emphasis on sector wide multiple compression and execution risk.

Together, these two Narratives bracket a fair value range of roughly US$57 to US$86, so your next step is to decide which set of assumptions about growth, risk and profitability feels closer to your own view of Block’s future, or whether your outlook sits somewhere in between.

If you want to see how other investors are framing that same question, along with the detailed numbers behind each storyline, See what the community is saying about Block.

Do you think there's more to the story for Block? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com