- If you are looking at FMC and wondering whether the current share price reflects its true worth, the valuation picture is the key question to focus on next.

- The stock last closed at US$17.64, with returns of 2.4% over 7 days, 25.6% over 30 days and 23.0% year to date. This is set against a 45.9% decline over 1 year, an 83.5% decline over 3 years and an 81.4% decline over 5 years.

- Recent attention on FMC has centered on how these mixed returns fit with the broader chemicals sector and shifts in investor sentiment about agricultural inputs. News coverage has highlighted how share prices across the space can adjust sharply when expectations around demand, costs or regulation change, giving useful context for FMC's recent moves.

- FMC currently holds a valuation score of 5 out of 6. This sets up a closer look at traditional valuation tools like discounted cash flow, multiples and peer comparisons, followed by a broader way to think about valuation that comes at the end of this article.

Find out why FMC's -45.9% return over the last year is lagging behind its peers.

Approach 1: FMC Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow model estimates what a business could be worth by projecting its future cash flows and discounting them back to today, so you can compare that value with the current share price.

For FMC, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections in US$. The latest twelve month free cash flow figure is a loss of about $161.4 million. Analyst inputs and subsequent extrapolations then feed into a ten year path where projected free cash flow reaches $345.1 million by 2035, with earlier years such as 2026 and 2028 sitting at $22.9 million and $177.5 million in absolute terms. Simply Wall St only uses direct analyst estimates for the nearer years and extrapolates the later ones.

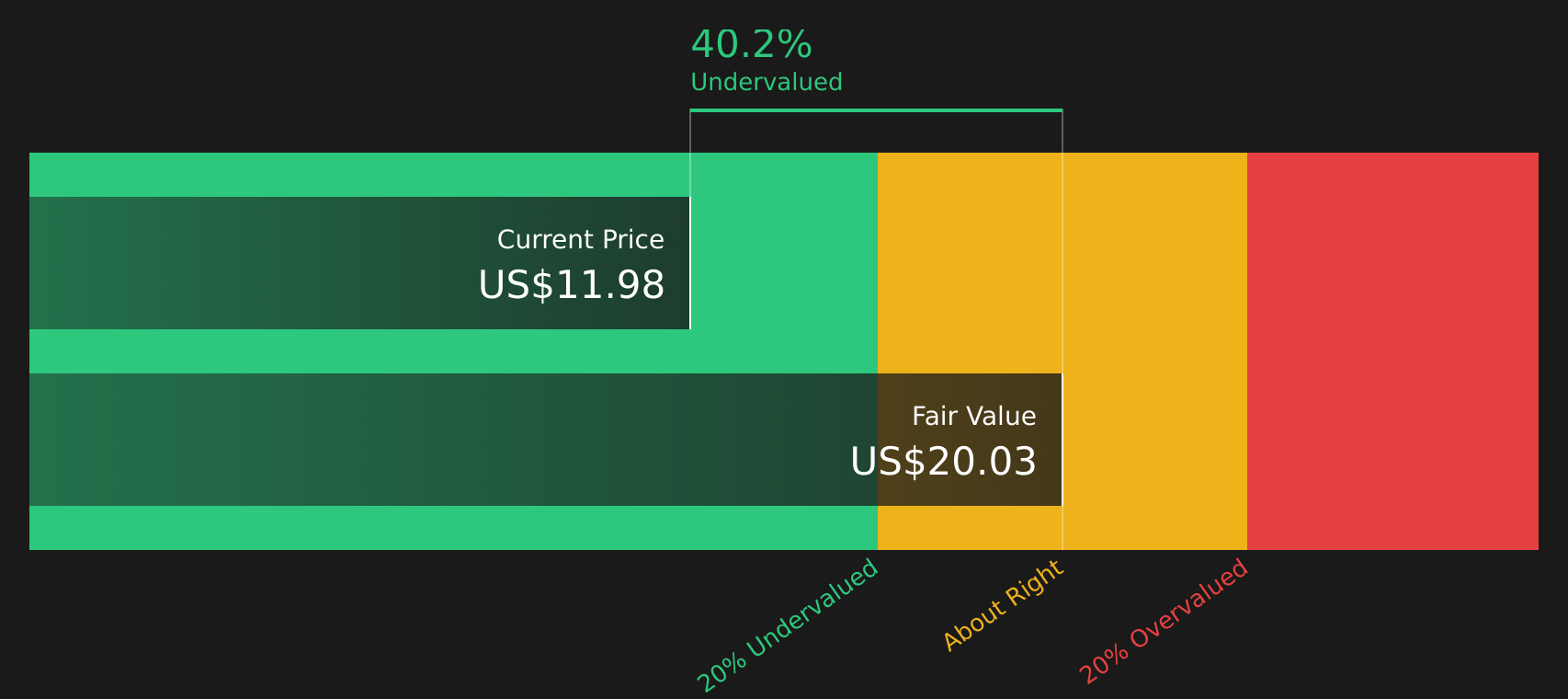

Bringing all of those projected cash flows back to today, the DCF model arrives at an estimated intrinsic value of about $23.32 per share. Against the recent share price of $17.64, this implies a 24.4% discount, which points to FMC trading below this DCF estimate.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests FMC is undervalued by 24.4%. Track this in your watchlist or portfolio, or discover 61 more high quality undervalued stocks.

Approach 2: FMC Price vs Sales

For FMC, price to sales is the preferred multiple. This can be useful when you want to compare companies on the value that the market is placing on each dollar of revenue. It is especially relevant when earnings are weak or volatile, because it focuses on the top line rather than profit figures that can swing with one off items.

In general, investors tend to accept a higher P/S ratio when they expect stronger growth or see lower risk in a business. A lower P/S is more typical where expectations are more muted or risks feel higher. The question is what looks reasonable for FMC today.

FMC is currently trading on a P/S of 0.64x. This sits below the Chemicals industry average P/S of 1.09x and also below the peer average of 1.25x. Simply Wall St’s Fair Ratio for FMC is 1.88x. This Fair Ratio is a proprietary estimate of what FMC’s P/S might be given factors such as its earnings growth profile, industry, profit margin, market cap and company specific risks.

Because it incorporates those company specific drivers, the Fair Ratio can provide a more tailored yardstick than a simple comparison with peers or the broad industry, which can mask important differences between businesses.

Comparing FMC’s actual P/S of 0.64x with the Fair Ratio of 1.88x suggests the shares are trading below this Fair Ratio estimate.

Result: UNDERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Upgrade Your Decision Making: Choose your FMC Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives pull everything together by letting you attach a clear story about FMC, such as whether it looks closer to a bearish fair value of US$13 or a more optimistic fair value of US$44.05 or US$74.11, to the numbers behind your assumptions on future revenue, earnings and margins. You can then link that story to a Fair Value and compare it with the current share price.

On Simply Wall St’s Community page, Narratives let you pick or adjust a view like the more cautious FMC case, where analysts model revenue growing 2.1% a year and earnings reaching US$212.2m by about 2029, or a more constructive case with higher growth and margins. You can then instantly see what Fair Value those paths imply and how that stacks up against today’s price.

Because Narratives update automatically when new earnings, news or guidance comes through, you can quickly see when the gap between your chosen Fair Value and the market price widens or closes. This can help you decide whether FMC looks closer to your bearish, base, or bullish story at any point in time.

For FMC however we'll make it really easy for you with previews of two leading FMC Narratives:

First up is a constructive, repair story that lines up with analysts who see meaningful upside if execution on cash flow, portfolio mix, and debt reduction plays out.

Fair value in this bullish narrative: US$18.12 per share.

At the last close of US$17.64, the price sits about 2.7% below this narrative fair value.

Analyst modeled revenue growth used in this view: about 5.47% a year.

- Analysts in this camp see demand for proprietary products and biologicals plus exposure to high growth regions as key drivers supporting revenue and margin repair over time.

- They focus on cost restructuring, manufacturing efficiencies, and portfolio shifts freeing up cash and improving profitability, with India changes intended to support a healthier balance sheet.

- The risks center on regulation, generic competition, pricing pressure, and execution on new launches, with the view that these are manageable if the company delivers on its plan.

On the other side is a more cautious narrative that takes the lower end of analyst targets and assumes the current price already bakes in too much optimism.

Fair value in this bearish narrative: US$13.00 per share.

At the last close of US$17.64, the price sits about 35.7% above this narrative fair value.

Analyst modeled revenue growth used in this view: about 2.07% a year.

- This group focuses on tighter regulation, shifts toward organic and regenerative farming, and dependence on a concentrated set of specialty products as headwinds for long term demand and pricing.

- They question whether R&D and new product spending is enough to offset patent risk, slower approvals, and rising development costs, which could cap earnings power.

- In this view, even with some improvement in earnings and margins, the market is seen as paying too much today relative to what these analysts consider a cautious fair value.

Taken together, these two FMC Narratives bracket a range of outcomes that you can use as reference points for your own assumptions on growth, regulation, and balance sheet progress.

Do you think there's more to the story for FMC? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com