Baron Capital's renewed interest in Ventas

Baron Capital’s recent decision to purchase additional Ventas (VTR) shares has put the senior housing focused real estate investment trust back in focus for investors, tying the move to fundamentals and an external growth pipeline.

See our latest analysis for Ventas.

The latest move by Baron Capital comes as Ventas trades at US$83.64, with a 90 day share price return of 10.5% and a 1 year total shareholder return of 35.7%. This suggests momentum has been building over the past year, while income has meaningfully supported overall returns.

If this kind of compounding story has your attention, it could be worth broadening your watchlist with other income focused opportunities such as 13 dividend fortresses

Ventas now trades at US$83.64 with a 26% intrinsic discount estimate and an 11% gap to the average analyst target. This raises a key question for you: is there still a buying opportunity here, or is future growth already priced in?

Most Popular Narrative: 10% Undervalued

Ventas closed at $83.64, while the most followed narrative pegs fair value at $92.95, framing Baron Capital’s move against a backdrop of earnings-focused growth expectations.

Ongoing active portfolio management, such as converting underperforming triple net assets to SHOP, acquisitions focused on high performing newer assets in strong demographic markets, and expanding relationships with best in class operators, creates a runway for outsized top line revenue and FFO per share growth.

Want to understand why this narrative supports a higher valuation? It leans on faster revenue gains, rising margins, and a punchy future earnings multiple.

Result: Fair Value of $92.95 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on execution, and persistent labor cost pressure or weaker than expected performance from senior housing operators could quickly challenge that optimistic setup.

Find out about the key risks to this Ventas narrative.

Another Angle On Ventas' Valuation

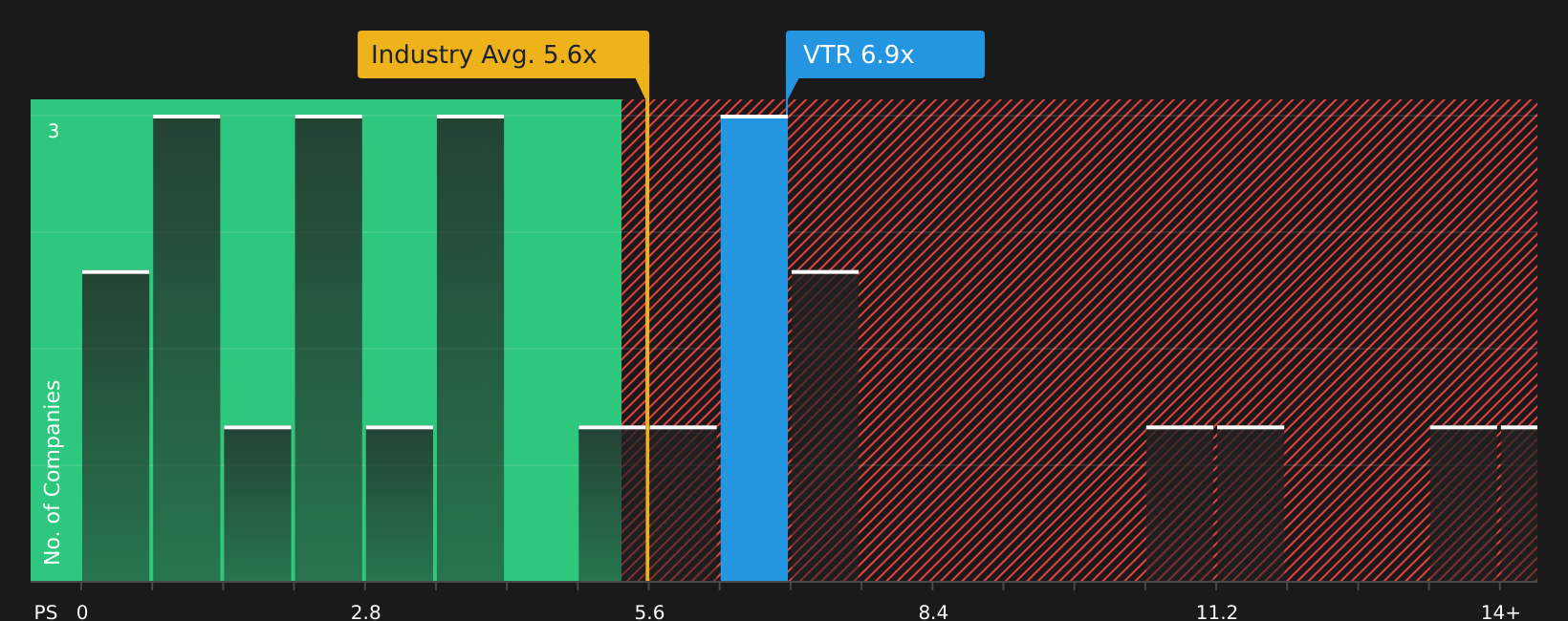

While one view leans on future earnings to argue Ventas is 10% below a fair value of $92.95, the current P/S ratio of 6.8x tells a different story. It sits above the Health Care REITs industry at 5.4x and above a fair ratio estimate of 5.9x, which points to valuation risk if sentiment cools.

This raises a practical question: do you focus on the upside implied by growth expectations, or pay more attention to today’s richer sales multiple and what it might mean for future returns?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With mixed signals on value and growth in play, it makes sense to look at the full picture yourself and decide how comfortable you are with the trade off between risk and reward. You can start with 3 key rewards and 4 important warning signs

Looking for more investment ideas?

If you want to give yourself more options than just one stock, use the screener to surface fresh ideas that match your goals before the next move passes you by.

- Target potential bargains with strong fundamentals by reviewing 61 high quality undervalued stocks that combine quality with attractive pricing.

- Strengthen your income stream by scanning 13 dividend fortresses that aim to pair higher yields with resilient payouts.

- Prioritise capital preservation and steadier rides by checking out 70 resilient stocks with low risk scores that score well on stability and downside risk.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com