- If you are wondering whether JetBlue Airways at US$5.04 is a bargain or a trap, the key question is how that price stacks up against what the business might be worth.

- The stock has returned 11.5% over the past week, 14.3% over the last month, and 9.8% year to date, with a 36.6% return over the past year. However, longer term 3 year and 5 year returns of negative 27.5% and negative 75.6% show that recent momentum sits on top of a tougher history.

- Recent coverage of JetBlue has focused on its position within the US airline industry and the challenges and opportunities that come with operating a lower cost carrier in a competitive market. This context helps frame why the stock can move sharply when sentiment around airlines or JetBlue's route and cost decisions shifts.

- JetBlue currently has a valuation score of 3 out of 6. The key is how traditional tools like P/E, P/S and discounted cash flow compare with a more complete way of thinking about value that will be covered at the end of this article.

Find out why JetBlue Airways's 36.6% return over the last year is lagging behind its peers.

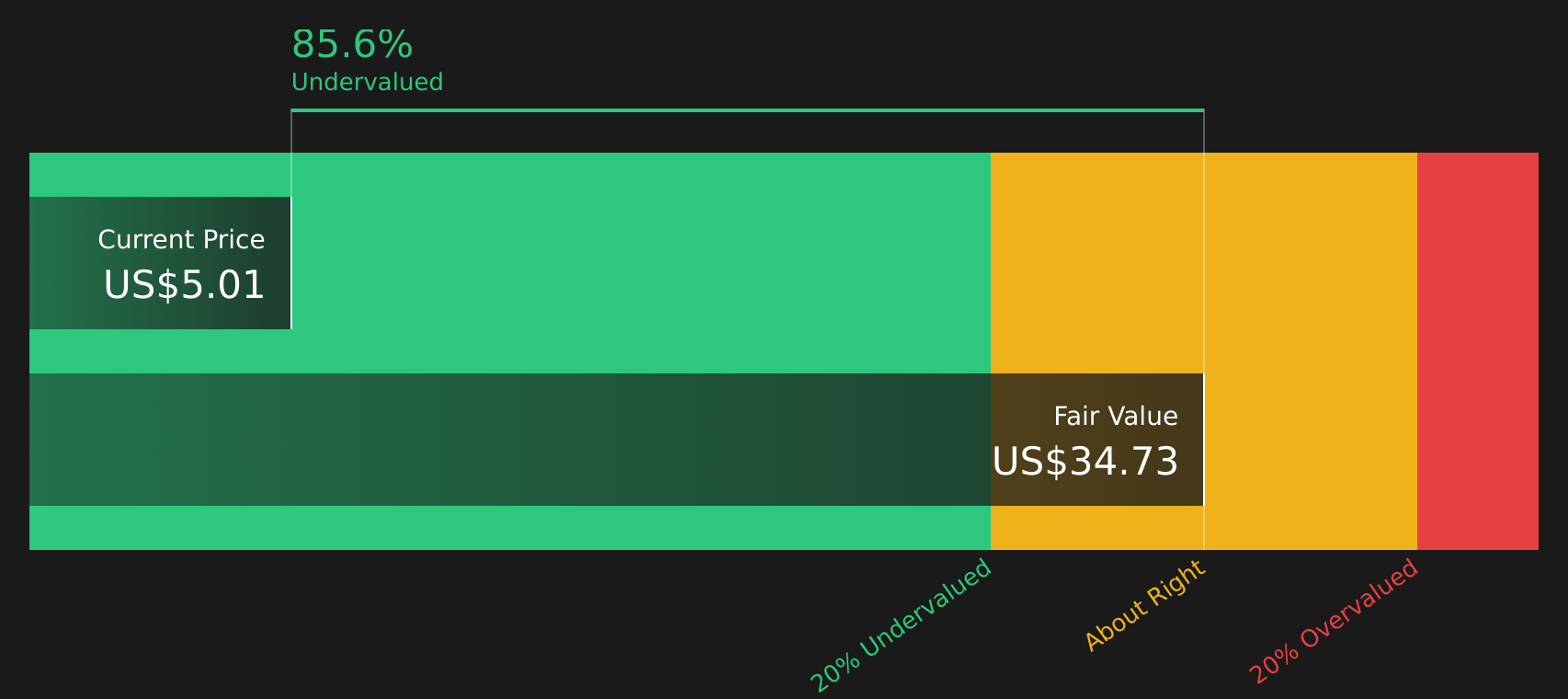

Approach 1: JetBlue Airways Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes estimated future cash flows and discounts them back to today to arrive at an estimate of what the entire business might be worth right now.

For JetBlue Airways, the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow is a loss of about $1.37b, and analysts supply detailed estimates out to 2028, with Simply Wall St extrapolating the projections further out to 2035. Within these projections, free cash flow moves from losses in the nearer years to a positive $89 million in 2028, and then to just over $444 million by 2035, all expressed in today's money after discounting.

Putting those discounted cash flows together, the DCF model arrives at an estimated intrinsic value of about $4.28 per share. Against the current share price of US$5.04, that implies the stock is roughly 17.8% overvalued based on this set of assumptions and projections.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests JetBlue Airways may be overvalued by 17.8%. Discover 64 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: JetBlue Airways Price vs Sales

For airlines and other companies where earnings can be volatile or negative, P/S is often a useful cross check because it focuses on what investors are paying for each dollar of revenue, rather than net profit.

In general, higher growth expectations and lower perceived risk tend to support a higher P/S multiple, while slower growth and higher risk usually align with a lower, more conservative range for what counts as a normal or fair ratio.

JetBlue Airways currently trades on a P/S of 0.21x. This sits below both the peer average of 0.52x and the broader Airlines industry average of about 0.55x, which suggests the market is assigning a lower value to JetBlue's revenue base compared with many competitors.

Simply Wall St's Fair Ratio for JetBlue, at 0.75x, is a proprietary estimate of what the P/S might be if factors such as earnings growth, profit margins, industry, market cap and stock specific risks were all reflected more fully in the valuation. This approach can be more tailored than a simple comparison with peers or the industry because it adjusts for the company’s own profile rather than assuming all airlines should trade on similar multiples.

Comparing the Fair Ratio of 0.75x with the actual P/S of 0.21x indicates that JetBlue Airways is trading below this modelled range.

Result: UNDERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your JetBlue Airways Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives are Simply Wall St's way of letting you attach a clear story to the numbers by combining your view on JetBlue Airways's future revenue, earnings and margins with an estimated fair value. You can then compare that to the current share price to decide if it looks high or low for you, all within an easy tool on the Community page that updates automatically when fresh news or earnings arrive. One investor might use the US$7.0 bullish fair value to build a JetBlue story around stronger demand and margin repair, while another leans on the US$3.0 bearish fair value to focus on regulatory costs, fuel and competition. This gives you a direct side by side view of how different assumptions translate into very different prices.

For JetBlue Airways, however, we’ll make it really easy for you with previews of two leading JetBlue Airways Narratives:

Fair value in this bullish narrative: US$6.38 per share

Implied discount to this fair value at US$5.04: about 21.0%

Revenue growth used in this narrative: 8.07%

- Assumes JetBlue steadily lifts margins and earnings by building on partnerships, digital sales, and loyalty revenue, with analysts using a 12.5% discount rate in their fair value work.

- Works off an updated US$6.38 fair value, with supporting analyst commentary that clusters price targets in the US$4 to US$5 range and focuses on sector demand into 2026.

- Highlights both upside drivers, such as brand strength and ancillary revenue, and risks around costs, regulation, and travel demand that readers are encouraged to weigh for themselves.

Fair value in this more cautious narrative: US$4.83 per share

Implied premium to this fair value at US$5.04: about 4.3%

Revenue growth used in this narrative: 7.62%

- Builds on a consensus analyst fair value of US$4.83 per share, using a 12.33% discount rate and modest margin improvement assumptions from a current loss making position.

- Leans on a relatively high implied future P/E multiple of about 112x low forecast earnings, which leaves less room for error if revenue or margins fall short.

- Flags practical risks, including demand uncertainty, fuel price exposure, rising labor costs, and competition, which could keep returns on capital and profitability under pressure.

If you want to see how other investors are framing the same numbers into different stories, and where you sit between these two JetBlue Airways views, it is worth reading the full narratives and comparing them with your own expectations before making any decision about the stock. See what the community is saying about JetBlue Airways

Do you think there's more to the story for JetBlue Airways? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com