- Insmed announced that its Phase 2b CEDAR study of brensocatib in adults with moderate to severe hidradenitis suppurativa failed to meet primary or secondary efficacy endpoints, leading the company to halt development of the drug for this indication despite a clean safety profile.

- An interesting outcome was that placebo patients saw a larger reduction in abscess and inflammatory nodule counts than either brensocatib dose, raising fresh questions about disease variability and trial design in hidradenitis suppurativa.

- We’ll now examine how discontinuing brensocatib in hidradenitis suppurativa reshapes Insmed’s investment narrative built around brensocatib’s broader potential.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 20 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Insmed Investment Narrative Recap

To own Insmed, you need to believe in the long term value of brensocatib in bronchiectasis and the company’s rare disease focus, supported by ARIKAYCE. The failed hidradenitis suppurativa study removes a peripheral use rather than the core bronchiectasis and CRS without nasal polyps catalysts, so the most important near term drivers and the key risk around FDA review timing remain largely unchanged.

The recent positive Phase 3b ENCORE data for ARIKAYCE, and Insmed’s plan to file an sNDA in the second half of 2026, now stand out even more as important clinical and regulatory milestones, especially as brensocatib’s HS program has been discontinued, concentrating investor attention on respiratory indications and upcoming regulatory interactions.

Yet, while respiratory indications stay in focus, investors should still be aware that FDA review timelines for brensocatib could...

Read the full narrative on Insmed (it's free!)

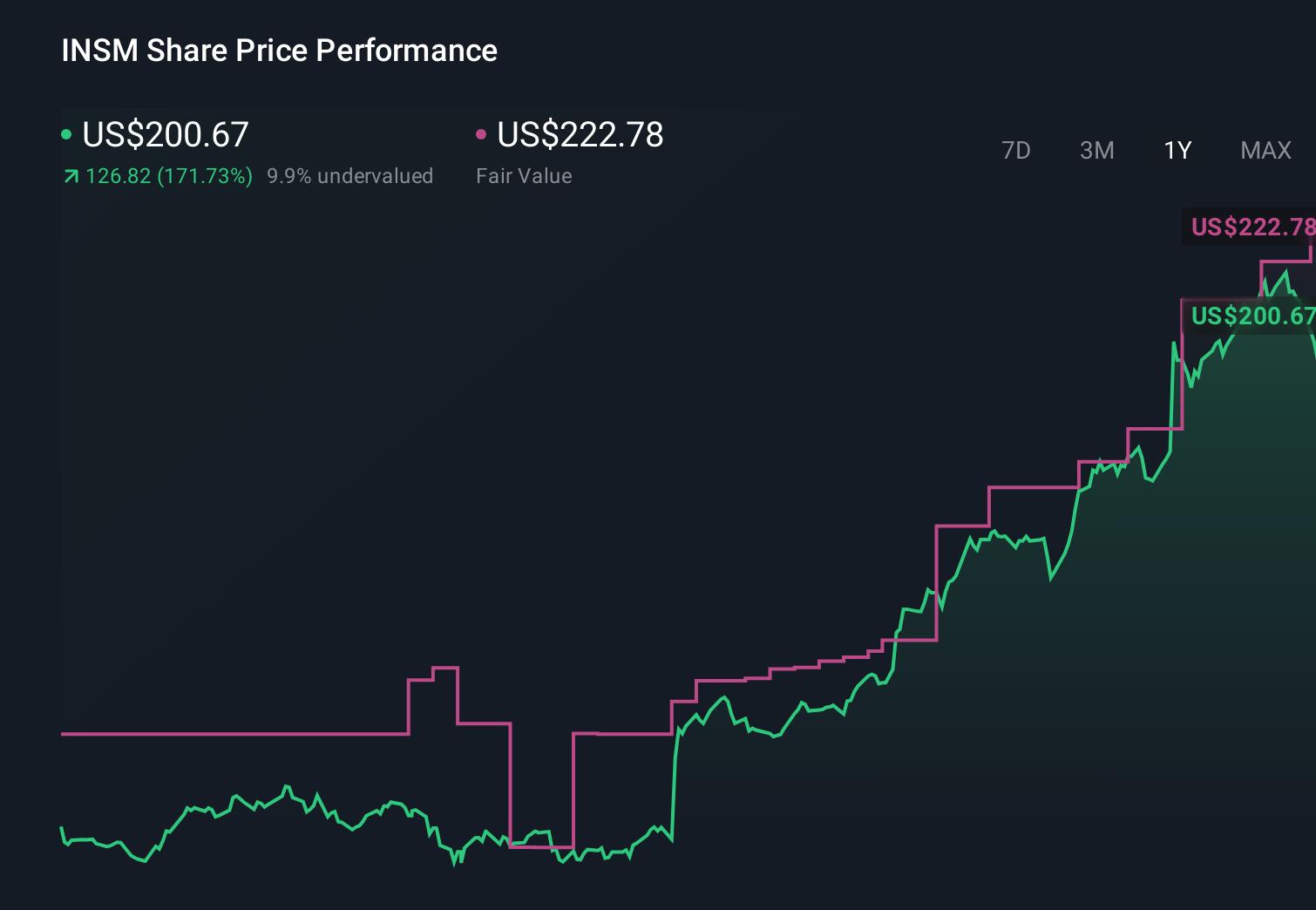

Insmed's narrative projects $3.9 billion revenue and $952.9 million earnings by 2029.

Uncover how Insmed's forecasts yield a $214.32 fair value, a 34% upside to its current price.

Exploring Other Perspectives

Four fair value estimates from the Simply Wall St Community span from about US$213 to over US$21,000 per share, showing very different expectations. Set against this, the recent brensocatib HS setback refocuses attention on regulatory timing for its lead respiratory use and what that could mean for Insmed’s future earnings profile.

Explore 4 other fair value estimates on Insmed - why the stock might be worth just $213.21!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Insmed research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Insmed research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Insmed's overall financial health at a glance.

Searching For A Fresh Perspective?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 28 companies in the world exploring or producing it. Find the list for free.

- Find 64 companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with 32 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com