- In March 2026, F.N.B. Corporation expanded its Capital Markets capabilities by adding municipal bond underwriting and tax‑exempt financing, delivered through its broker‑dealer subsidiary FNB America Securities LLC to support governments and nonprofits with longer‑term, relatively low‑cost project funding.

- This move, alongside F.N.B.’s growing use of advanced data analytics in capital markets, underscores how the bank is deepening fee‑based services while enhancing support for municipal clients.

- Next, we’ll examine how this move into municipal bond underwriting could reshape F.N.B.’s investment narrative around fee income and capital markets expansion.

Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

F.N.B Investment Narrative Recap

To own F.N.B., you need to believe in its ability to grow a diversified, tech-enabled regional banking franchise while managing concentrated regional exposure, deposit competition and CRE credit risk. The move into municipal bond underwriting modestly supports the key near term catalyst of expanding fee-based capital markets income, but does not materially change the main risks tied to regional concentration or technology spend.

The March 2026 launch of municipal bond underwriting builds directly on the 2025 acquisition of Raptor Partners, which broadened F.N.B.'s investment banking reach. Together, these moves reinforce the catalyst around growing noninterest income through an expanded Capital Markets platform and may gradually reduce reliance on traditional spread income, even as the bank continues to invest in digital tools like its eStore and AI driven insights.

Yet behind this expanding Capital Markets story, investors should also be aware of the risk that...

Read the full narrative on F.N.B (it's free!)

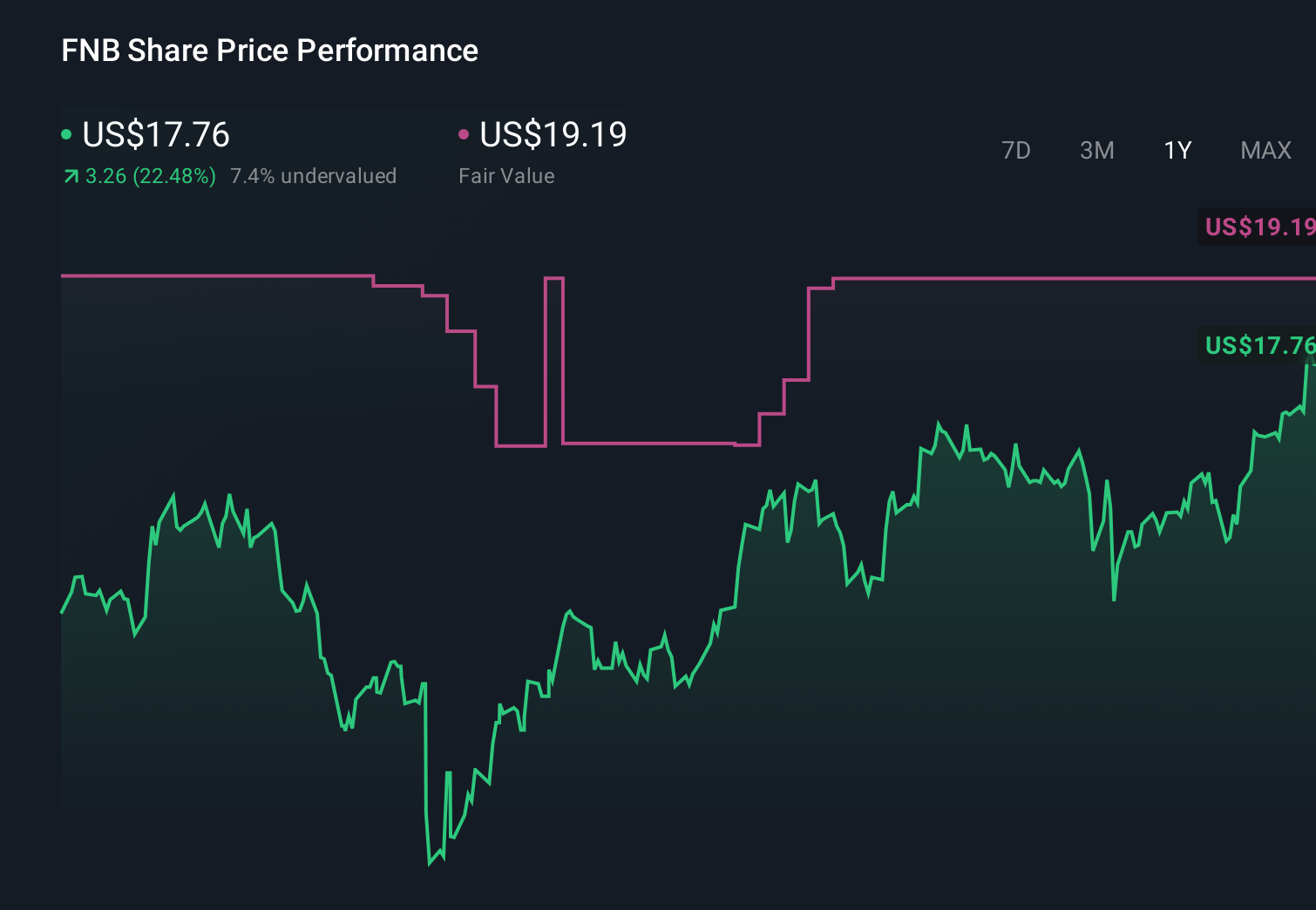

F.N.B's narrative projects $2.2 billion revenue and $761.3 million earnings by 2029.

Uncover how F.N.B's forecasts yield a $20.06 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Four fair value estimates from the Simply Wall St Community span about US$20 to over US$63 per share, showing how far apart individual views can be. As you weigh those opinions against F.N.B.'s push into fee based Capital Markets and ongoing digital investment, it is worth exploring several perspectives on how these shifts could influence future profitability and risk.

Explore 4 other fair value estimates on F.N.B - why the stock might be worth just $20.06!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your F.N.B research is our analysis highlighting 5 key rewards that could impact your investment decision.

- Our free F.N.B research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate F.N.B's overall financial health at a glance.

Curious About Other Options?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 28 best rare earth metal stocks of the very few that mine this essential strategic resource.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Capitalize on the AI infrastructure supercycle with our selection of the 36 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com