- Wondering if Oracle at US$143.66 still offers value or if most of the easy gains are behind it? This article walks through what the current price may imply about the stock.

- The share price has seen a 1.1% decline over the last 7 days and a 5.2% decline over the last 30 days, while still showing a 4.2% return over 1 year and a 100.1% return over 5 years.

- These moves are landing at a time when Oracle continues to attract attention around its position in software and cloud infrastructure, with ongoing headlines about its role in supporting large scale enterprise workloads and database migrations. For investors, that mix of long term relevance and recent share price softness raises questions about whether sentiment or fundamentals are driving the latest moves.

- Oracle currently has a valuation score of 5 out of 6. This means most of the checks used here suggest the stock may be trading below what certain models imply. The next sections will compare those valuation approaches, while keeping one extra, possibly more useful, way of thinking about value for the end of the article.

Approach 1: Oracle Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company could be worth today by projecting its future cash flows and then discounting those back to a single present value figure. It focuses on the cash that might be available to shareholders rather than accounting profits.

For Oracle, the model used here is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections in US$. The latest twelve months free cash flow is a loss of about US$2.2b. Analyst inputs and extrapolated estimates then project future free cash flows, with one example projection of US$29.9b in 2030 and a series of annual forecasts in between.

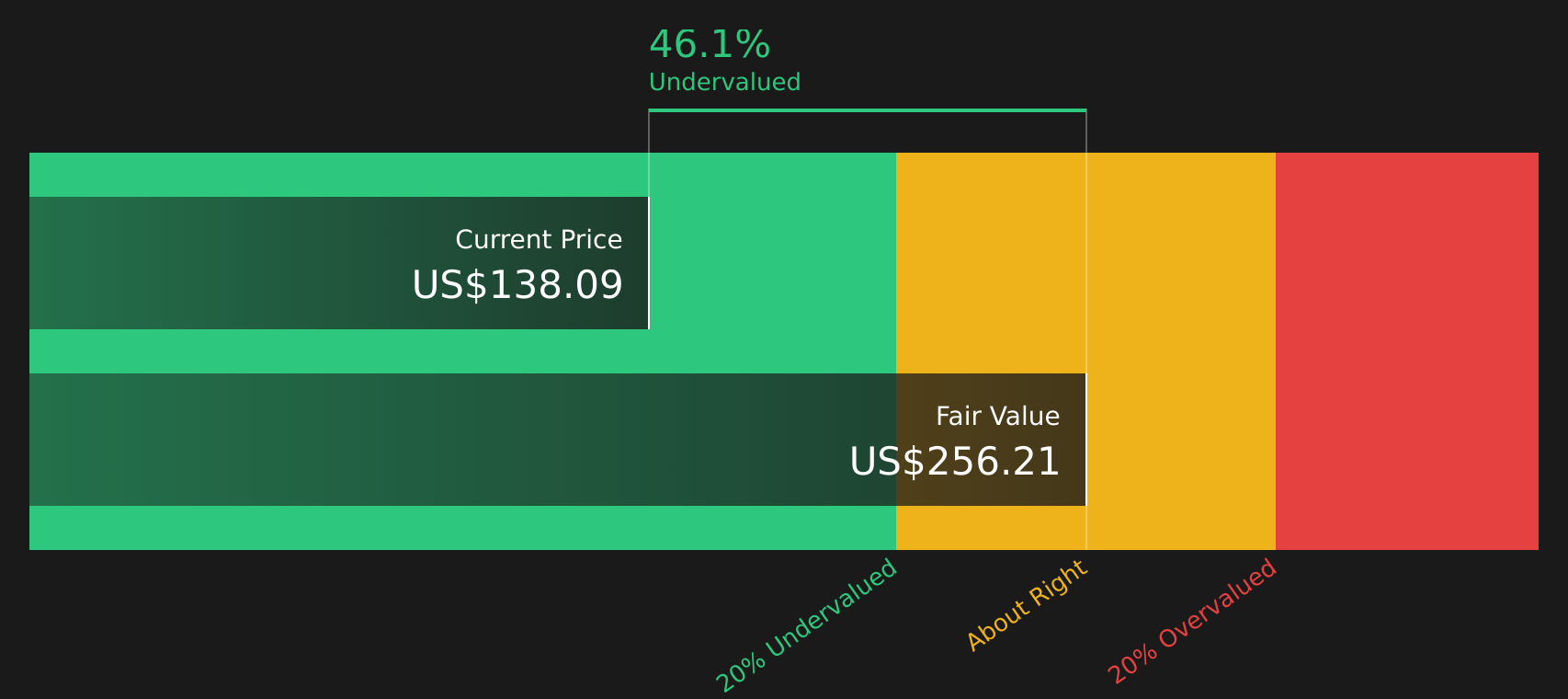

When all those projected cash flows are discounted back to today, the model arrives at an estimated intrinsic value of about US$257.95 per share. Compared with a current share price of US$143.66, this particular DCF output suggests the stock is 44.3% undervalued on these assumptions and inputs.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Oracle is undervalued by 44.3%. Track this in your watchlist or portfolio, or discover 64 more high quality undervalued stocks.

Approach 2: Oracle Price vs Earnings

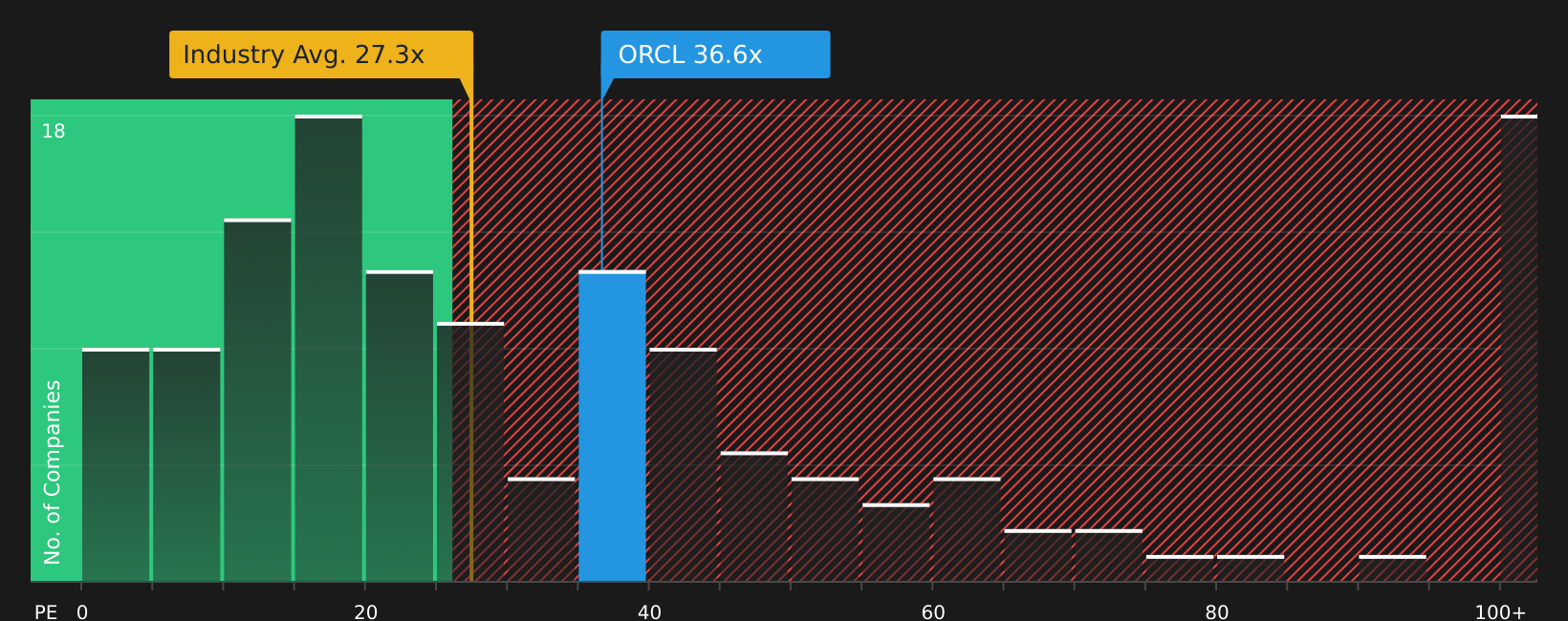

For profitable companies, the P/E ratio is a useful shorthand for how much investors are paying for each dollar of current earnings. It connects directly to what you see on the income statement and is widely used, which makes comparisons more intuitive.

What counts as a “normal” P/E depends on how quickly earnings are expected to change and how risky those earnings are perceived to be. Higher growth and lower risk can justify a higher P/E, while lower growth or higher risk often align with a lower P/E. Oracle currently trades on a P/E of 25.5x, compared with the Software industry average of about 28.5x and a peer group average of 56.1x.

Simply Wall St’s “Fair Ratio” is a proprietary P/E estimate that reflects factors such as earnings growth, profit margins, industry, market cap and company specific risks. Because it pulls these inputs together, it can be more tailored than a simple comparison with peers or an industry average, which may have very different growth and risk profiles. For Oracle, the Fair Ratio is 56.1x, well above the current 25.5x, which in this framework indicates that the shares screen as undervalued.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Oracle Narrative

Earlier the article mentioned that there is an even better way to understand valuation. This is where Narratives come in, a simple tool on Simply Wall St’s Community page that lets you attach your own story about Oracle to the numbers. You can link your view on its AI infrastructure role, cloud growth, risks and margins to a clear forecast for revenue, earnings and cash flows. This then produces a Fair Value you can compare directly with the current price to guide buy or sell decisions. Narratives include updates that adjust automatically as new news or earnings arrive, and a wide range of existing Oracle Narratives already span from very optimistic fair values around US$359.59, with assumptions such as revenue reaching about US$169.8b and earnings of US$38.7b by 2029 on a 37.8x P/E, through to more cautious fair values around US$119.97 to US$155.00 that instead anchor on lower or more conservative earnings paths and margin assumptions.

For Oracle however we will make it really easy for you with previews of two leading Oracle Narratives:

Fair value in this narrative: US$389.81 per share

Implied discount to this fair value at US$143.66: about 63%

Revenue growth assumption: 28%

- Frames Oracle as an AI infrastructure partner for demanding workloads, highlighting superclusters, the OpenAI relationship and very large data center projects.

- Points to a very large remaining performance obligations figure and strong AI related demand as key supports for long term revenue and earnings targets across infrastructure, databases and applications.

- Flags practical risks such as capacity build out, supply constraints, execution challenges and scepticism around AI projects as important watchpoints.

Fair value in this narrative: US$119.97 per share

Implied premium to this fair value at US$143.66: about 20%

Revenue growth assumption: 4.55%

- Emphasises Oracle’s large existing database customer base and high margins, while treating its role in AI infrastructure and cloud as material but more measured in scale.

- Works through a simple scenario where revenue and earnings step up over time. It then applies a 25x P/E multiple to arrive at a long term valuation range around US$180 to US$200.

- Stresses competition from larger cloud providers and the capital intensity of new data centers as key risks that could justify a more conservative fair value today.

If this kind of side by side view helps sharpen your own view on Oracle, it can be useful to see how many other narratives line up with each side and what assumptions they lean on most heavily.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Oracle on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Oracle? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com