- Everspin Technologies recently announced a 10-year agreement, extendable in 2-year increments, to use Microchip Technology’s Oregon fabrication facility to expand onshore production of MRAM and Tunnel Magnetoresistive sensor products while retaining its own intellectual property and processes.

- This long-term foundry arrangement adds an ITAR-compliant, onshore second source for advanced memory and sensor wafers, underscoring Microchip’s role as an enabler of secure, domestically manufactured semiconductor capacity.

- We’ll now examine how Microchip’s foundry role in Everspin’s onshore MRAM expansion could influence its investment narrative and manufacturing profile.

Explore 24 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Microchip Technology Investment Narrative Recap

To own Microchip Technology, you have to believe it can turn its embedded control and analog strengths into durable, profitable growth while managing its leverage and still-elevated inventories. The Everspin foundry deal modestly supports that case near term by utilizing existing fab capacity, but it does not directly resolve Microchip’s biggest current risks around debt load, inventory normalization, and associated margin pressure.

Among recent announcements, the February 2026 guidance for Q4 FY2026 stands out, with Microchip projecting US$1.240 billion to US$1.280 billion in net sales and a 13.5% to 15.0% operating margin. That outlook framed the key catalyst of margin recovery after underutilization charges; the new Everspin agreement could become incrementally helpful to fab efficiency over time, but its first products are only expected in the second half of 2027.

Yet behind this improving utilization story, investors should also be aware of how Microchip’s high net debt and undercovered dividend could become far more problematic if...

Read the full narrative on Microchip Technology (it's free!)

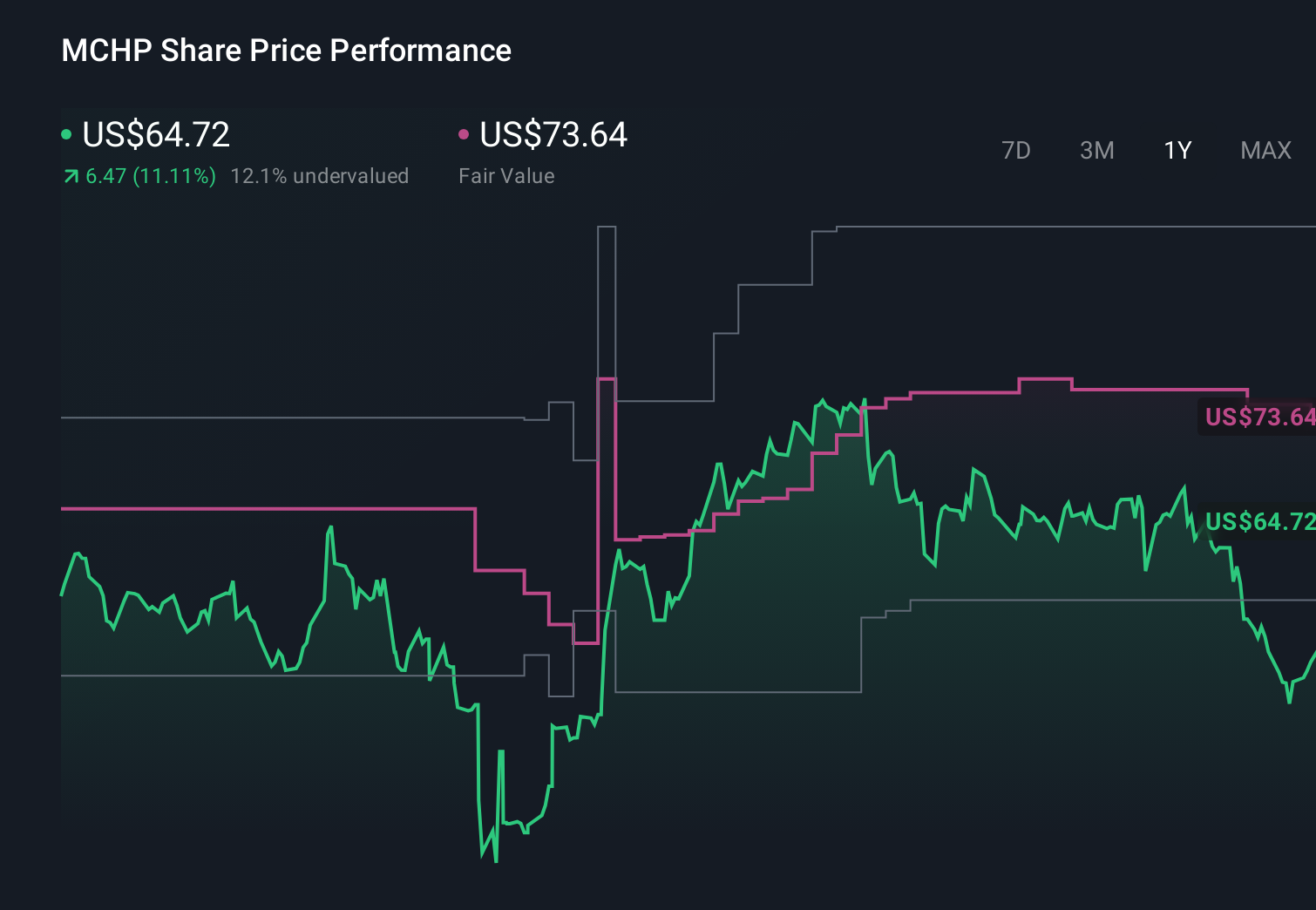

Microchip Technology's narrative projects $7.3 billion revenue and $1.9 billion earnings by 2029.

Uncover how Microchip Technology's forecasts yield a $86.67 fair value, a 22% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already expecting revenues near US$8.4 billion and about US$2.1 billion in earnings by 2028, so compared with concerns around de globalization and complex supply chain shifts, this new long term, ITAR capable foundry role with Everspin could either reinforce or challenge that bullish path, and it is worth comparing these very different views before you decide which narrative feels more realistic.

Explore 5 other fair value estimates on Microchip Technology - why the stock might be worth as much as 53% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Microchip Technology research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Microchip Technology research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Microchip Technology's overall financial health at a glance.

Curious About Other Options?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Rare earth metals are the new gold rush. Find out which 27 stocks are leading the charge.

- Uncover the next big thing with 32 elite penny stocks that balance risk and reward.

- Find 62 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com