- In late March 2026, Royal Caribbean Group and Bank of America launched the Royal ONE and Royal ONE Plus tri-branded Visa Signature credit cards, giving guests a new way to earn and redeem rewards across Royal Caribbean, Celebrity Cruises, and Silversea with tiered points and travel perks.

- This move deepens Royal Caribbean Group’s loyalty ecosystem by linking its brands under a single rewards framework, aiming to boost repeat business through richer, more flexible benefits for frequent cruisers.

- Next, we’ll examine how this expanded loyalty and credit card offering could influence Royal Caribbean’s investment narrative and long-term demand profile.

Capitalize on the AI infrastructure supercycle with our selection of the 36 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

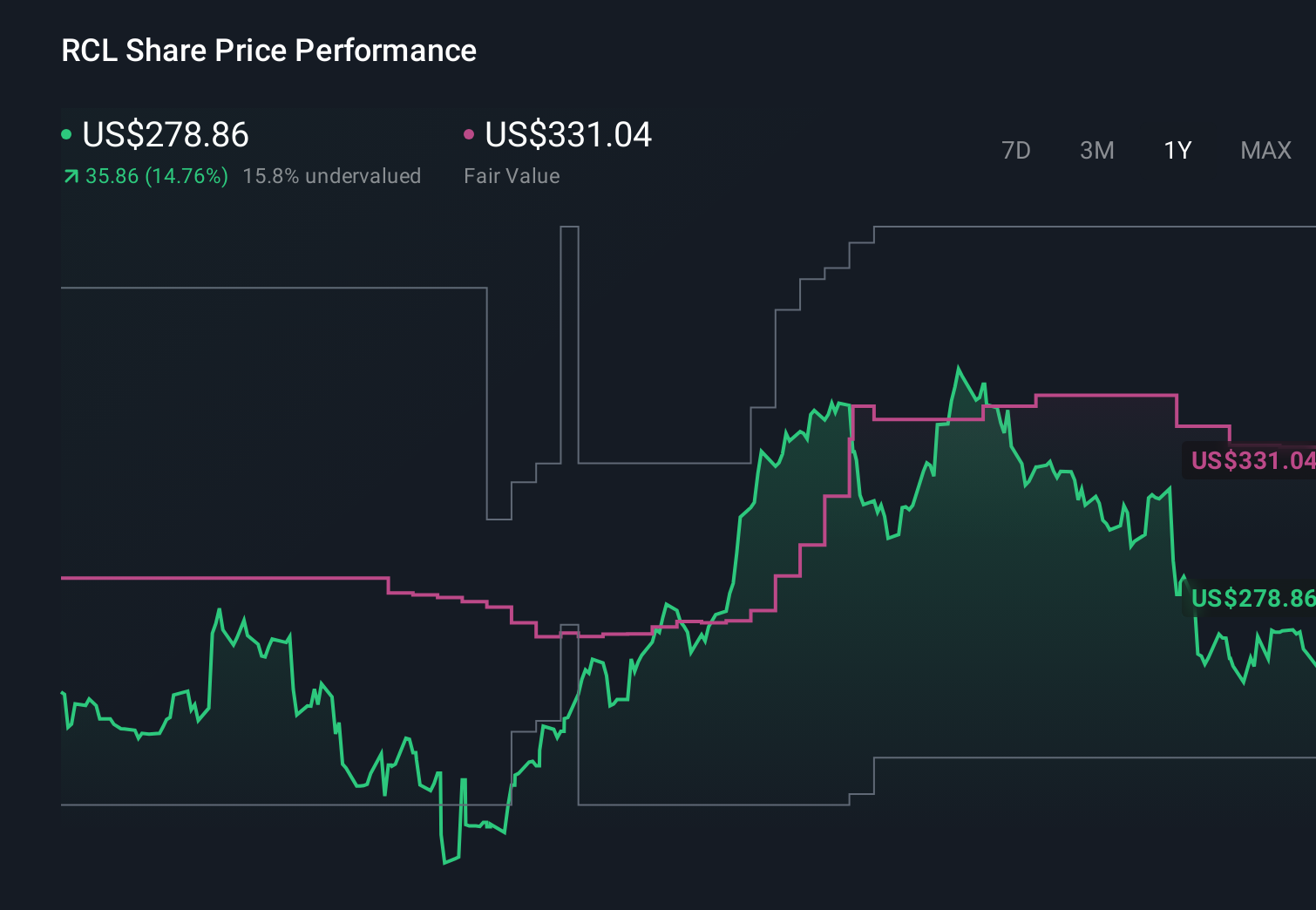

Royal Caribbean Cruises Investment Narrative Recap

To own Royal Caribbean, you need to believe cruising remains a compelling vacation choice despite economic uncertainty and fuel and currency volatility. The new Royal ONE credit cards strengthen the company’s loyalty engine, but they do not change that the key short term swing factor is demand resilience and pricing power, while the biggest near term risk remains any pullback in consumer discretionary spending or a slowdown in close in bookings.

The launch of the tri branded Royal ONE and Royal ONE Plus cards ties directly into Royal Caribbean’s existing loyalty initiatives, such as Status Match and Points Choice, by giving frequent guests more ways to earn and redeem across Royal Caribbean, Celebrity Cruises, and Silversea. This fits with the broader catalyst of deeper loyalty programs supporting repeat bookings and onboard spend, even if macro conditions or fuel costs become more challenging.

But while loyalty looks stronger than ever, investors should still be aware that...

Read the full narrative on Royal Caribbean Cruises (it's free!)

Royal Caribbean Cruises' narrative projects $22.4 billion revenue and $5.9 billion earnings by 2028. This requires 9.2% yearly revenue growth and about a $2.3 billion earnings increase from $3.6 billion.

Uncover how Royal Caribbean Cruises' forecasts yield a $362.04 fair value, a 31% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already cautious, projecting around US$21.9 billion of revenue and US$5.9 billion of earnings by 2028, and they highlight how views on fuel costs, debt levels and loyalty driven growth can diverge sharply, so it is worth exploring how this new credit card program might shift both the optimistic and more pessimistic narratives before you decide where you stand.

Explore 7 other fair value estimates on Royal Caribbean Cruises - why the stock might be worth as much as 60% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Royal Caribbean Cruises research is our analysis highlighting 5 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Royal Caribbean Cruises research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Royal Caribbean Cruises' overall financial health at a glance.

Curious About Other Options?

Our top stock finds are flying under the radar-for now. Get in early:

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

- We've uncovered the 11 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com