Event context and recent share performance

W. R. Berkley (WRB) continues to draw attention after a mixed stretch for the stock, with a modest 1-day decline, a gain over the past week, and negative returns over the month and past 3 months.

See our latest analysis for W. R. Berkley.

At a share price of $67.21, W. R. Berkley has seen short term share price momentum soften this year, even as its 1 year and multi year total shareholder returns remain firmly positive.

If you are rethinking where to put fresh capital to work, it can be helpful to compare WRB with other insurance names and broader financials that offer different risk and return profiles, including those that are more growth oriented or income focused.

To broaden your watchlist beyond a single insurer, now could be a good time to scan for other financial names using our screener of resilient businesses, starting with 19 top founder-led companies

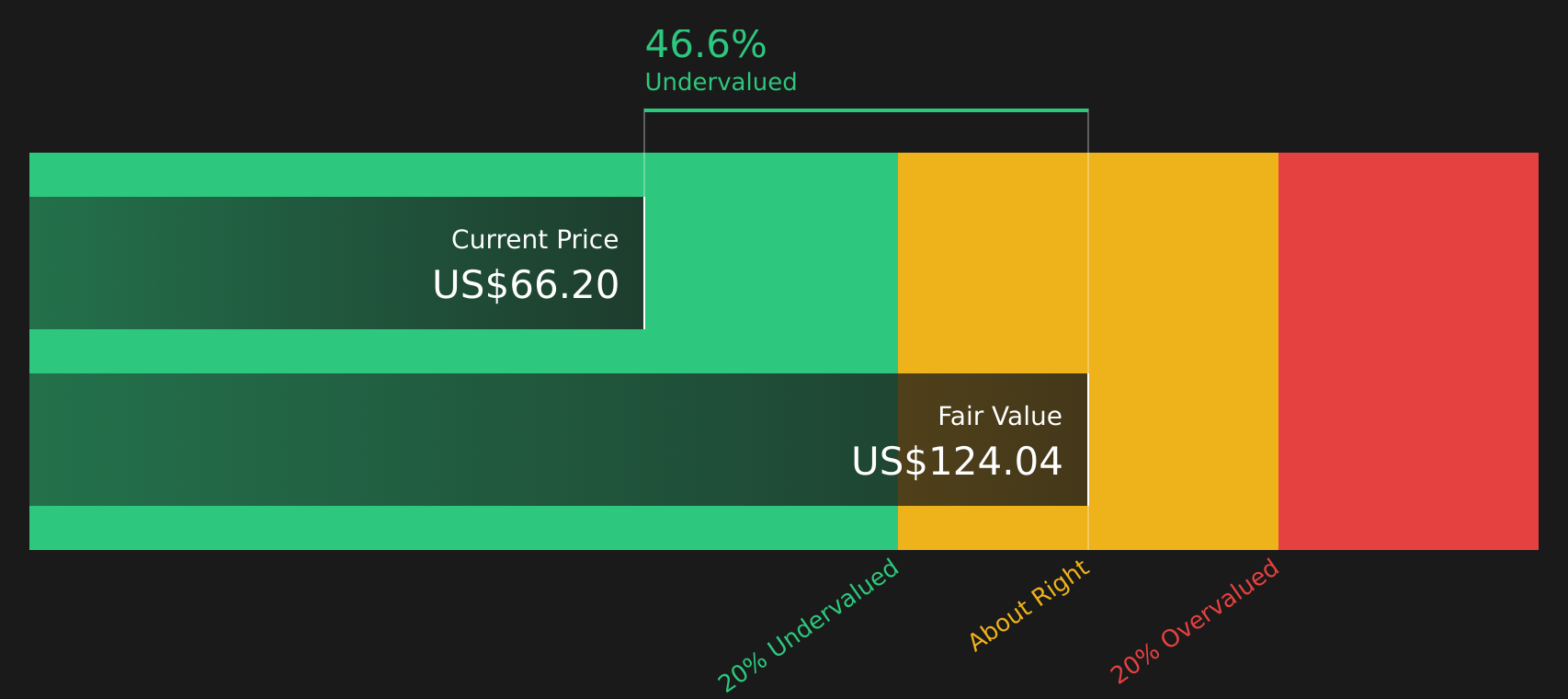

With WRB trading near analyst targets yet showing a roughly 46% intrinsic discount, the key question is whether the stock is quietly undervalued or whether the market already reflects its future growth potential.

Most Popular Narrative: 2% Undervalued

At $67.21 versus a narrative fair value of $68.33, W. R. Berkley screens as slightly undervalued, with the valuation anchored on a detailed cash flow and earnings framework using a 6.98% discount rate.

Prudent capital management, shown by a growing investment portfolio benefitting from higher new money yields and conservative reserving, is increasing investment income and book value per share, laying a foundation for higher long-term earnings and the potential for resumed share buybacks.

Curious what sits under that small discount to fair value? The narrative leans heavily on steady margins, measured revenue assumptions, and a future earnings multiple that needs to hold up. The key is how these inputs interact over time, not any single headline number.

Result: Fair Value of $68.33 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on underwriting discipline holding up, as softer commercial and reinsurance pricing or higher loss trends could quickly pressure margins and challenge those valuation assumptions.

Find out about the key risks to this W. R. Berkley narrative.

Another angle on valuation

The SWS DCF model paints a very different picture from the narrative fair value, with W. R. Berkley at $67.21 compared with an estimated future cash flow value of $125.55. That gap suggests the market could be heavily discounting long term cash generation, or the model is simply too optimistic. Which side do you trust more?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

With mixed signals across the valuations and sentiment clearly divided, it makes sense to move quickly, review the numbers yourself, and weigh both sides using the 2 key rewards and 1 important warning sign

Looking for more investment ideas?

If W. R. Berkley is on your radar, now is the time to round out your watchlist with a few focused idea lists that target very different strengths.

- Spot potential deep value opportunities early by scanning our list of 62 high quality undervalued stocks before the crowd catches on.

- Strengthen the quality of your portfolio by filtering for companies using the solid balance sheet and fundamentals stocks screener (40 results) so weaker balance sheets do not quietly drag on returns.

- Get ahead of the market by reviewing a screener containing 24 high quality undiscovered gems that other investors may be overlooking right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com