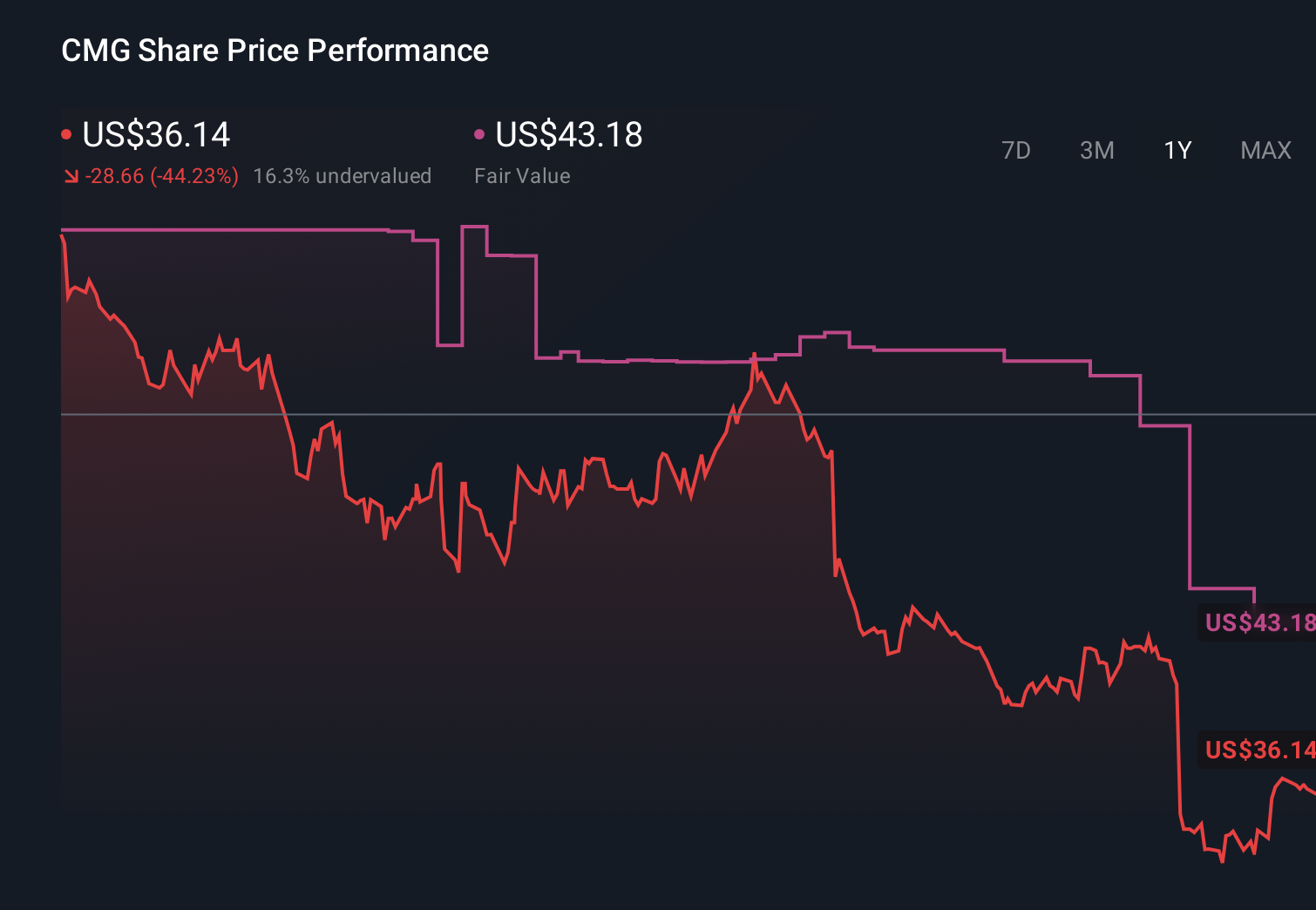

- In recent days, Chipotle Mexican Grill received an analyst upgrade to Outperform despite ongoing sales pressures, cautious consumer spending, and intense competition across the restaurant industry.

- At the same time, management is pressing ahead with plans to open 350 to 370 new restaurants in 2026, underscoring a commitment to expansion even as comparable sales remain under pressure.

- Now we’ll examine how this analyst upgrade, alongside Chipotle’s aggressive new restaurant expansion, influences the company’s broader investment narrative.

Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

Chipotle Mexican Grill Investment Narrative Recap

To own Chipotle, you need to believe that management can turn around weak comparable sales while still earning solid returns on a fast expanding store base. The Mizuho upgrade does not change the core near term story: the key catalyst is a credible recovery in traffic and comps, while the biggest risk is that ongoing consumer pullbacks and competition keep sales sluggish even as Chipotle commits sizable capital to hundreds of new openings.

The most relevant recent announcement here is Chipotle’s plan to open 350 to 370 new restaurants in 2026, including a 20 percent expansion in the UK. This ties the upgrade directly to the company’s “Recipe for Growth” playbook, where new units are doing most of the heavy lifting while existing restaurant performance is under strain, making execution on these openings central to whether the stock’s investment case holds up.

But beneath the expansion headlines, one risk investors should really keep in mind is how negative comps and cautious spending could interact with rising build costs if …

Read the full narrative on Chipotle Mexican Grill (it's free!)

Chipotle Mexican Grill's narrative projects $16.1 billion revenue and $2.0 billion earnings by 2029. This requires 10.5% yearly revenue growth and about a $0.5 billion earnings increase from $1.5 billion today.

Uncover how Chipotle Mexican Grill's forecasts yield a $44.59 fair value, a 30% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts tell a much tougher story, assuming profit margins drift toward 11.9 percent and earnings only reach about US$1.9 billion by 2028, which contrasts sharply with today’s bullish upgrade and raises fair questions about how aggressive unit growth could backfire if international execution or U.S. traffic do not improve.

Explore 16 other fair value estimates on Chipotle Mexican Grill - why the stock might be worth as much as 54% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Chipotle Mexican Grill research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Chipotle Mexican Grill research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Chipotle Mexican Grill's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Outshine the giants: these 20 early-stage AI stocks could fund your retirement.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- We've uncovered the 11 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com