The market has climbed 3.4% in the last 7 days and an impressive 30% over the past year, with earnings projected to grow annually by 16%. In light of these robust market conditions, identifying stocks with strong financials becomes crucial for investors looking to capitalize on growth opportunities. Although often considered a relic, penny stocks still hold potential when backed by solid fundamentals, offering a unique blend of value and growth that might not be found in larger companies.

Top 10 Penny Stocks In The United States

| Name | Share Price | Market Cap | Rewards & Risks |

| WM Technology (MAPS) | $0.4011 | $69.45M | ✅ 3 ⚠️ 5 View Analysis > |

| LexinFintech Holdings (LX) | $2.19 | $375.23M | ✅ 3 ⚠️ 2 View Analysis > |

| FinVolution Group (FINV) | $4.97 | $1.31B | ✅ 4 ⚠️ 1 View Analysis > |

| Tuniu (TOUR) | $0.7079 | $81.81M | ✅ 2 ⚠️ 2 View Analysis > |

| Information Services Group (III) | $3.11 | $194.03M | ✅ 3 ⚠️ 1 View Analysis > |

| Golden Growers Cooperative (GGRO.U) | $5.00 | $77.45M | ✅ 2 ⚠️ 5 View Analysis > |

| Niagen Bioscience (NAGE) | $4.48 | $369.14M | ✅ 3 ⚠️ 1 View Analysis > |

| Cricut (CRCT) | $4.14 | $897.95M | ✅ 2 ⚠️ 2 View Analysis > |

| LifeVantage (LFVN) | $4.02 | $52.12M | ✅ 4 ⚠️ 3 View Analysis > |

| SIGA Technologies (SIGA) | $7.80 | $328.13M | ✅ 2 ⚠️ 1 View Analysis > |

Click here to see the full list of 361 stocks from our US Penny Stocks screener.

Let's dive into some prime choices out of the screener.

Ceragon Networks (CRNT)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: Ceragon Networks Ltd. offers wireless transport solutions for cellular operators and other wireless service providers across various global regions, with a market cap of approximately $206.75 million.

Operations: The company generated $338.73 million in revenue from its role as a global innovator and leading solutions provider of wireless transport.

Market Cap: $206.75M

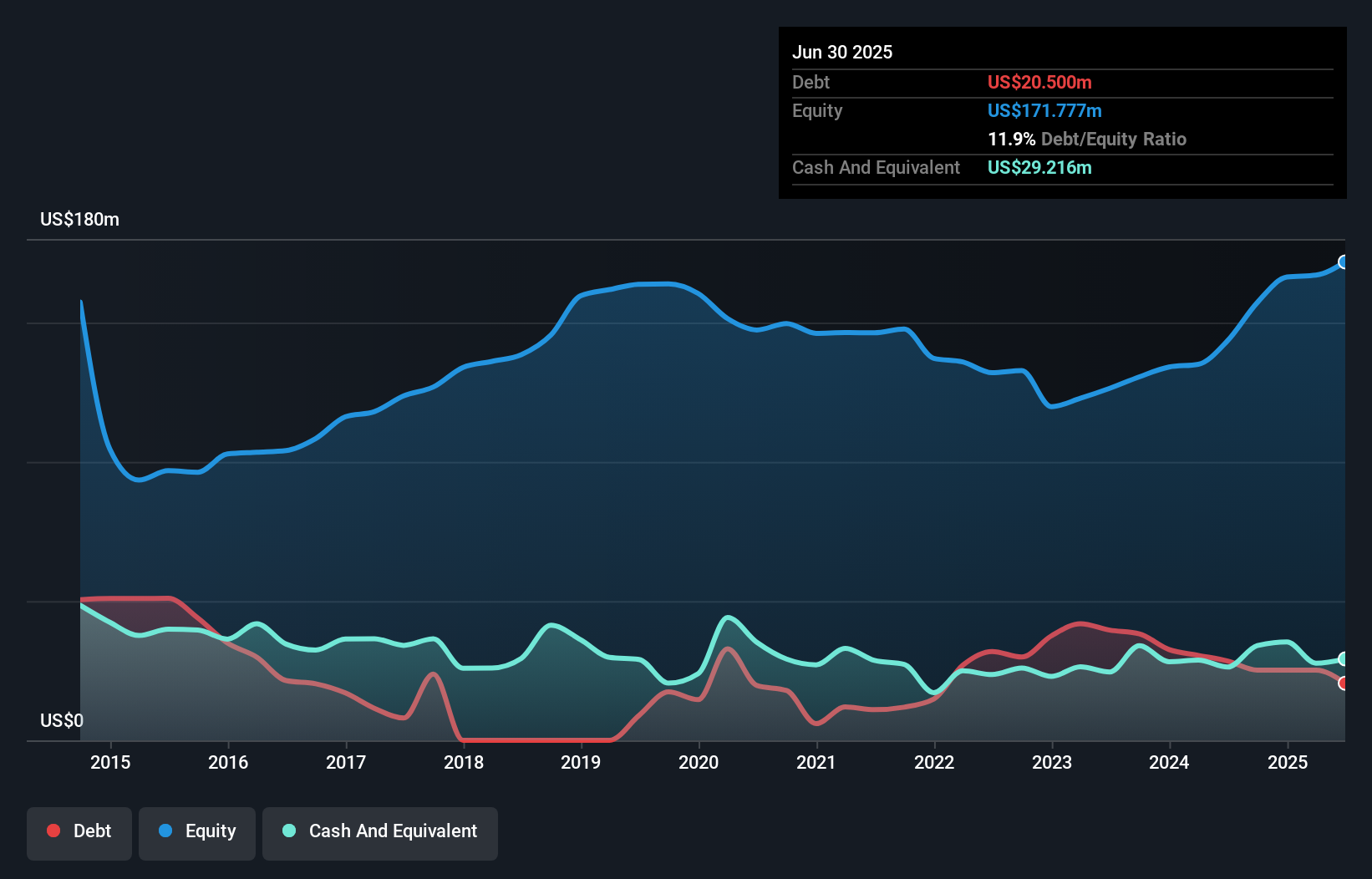

Ceragon Networks Ltd. is navigating the challenges of being unprofitable, with a recent net loss of US$2.09 million for 2025, though it maintains a strong cash position with short-term assets exceeding both its short and long-term liabilities. Despite the current lack of profitability, the company forecasts significant revenue growth for 2026 between US$355 million and US$385 million and expects earnings to grow by 90.75% annually. Ceragon's management team is seasoned, with an average tenure of 4.9 years, suggesting stability in leadership amidst financial volatility and industry competition.

- Take a closer look at Ceragon Networks' potential here in our financial health report.

- Evaluate Ceragon Networks' prospects by accessing our earnings growth report.

Caesarstone (CSTE)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: Caesarstone Ltd. designs, develops, manufactures, and sells engineered stone and porcelain products under various brands across multiple regions including the United States, Canada, Latin America, Australia, Asia, Europe, the Middle East and Africa, and Israel with a market cap of $47.02 million.

Operations: The company generates $397.23 million in revenue from its building products segment.

Market Cap: $47.02M

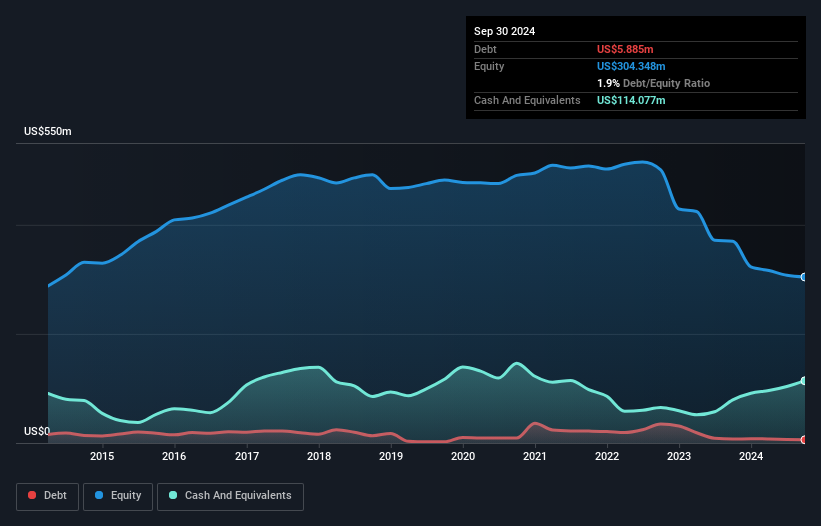

Caesarstone Ltd. faces financial challenges, with a net loss of US$137.47 million for 2025 and declining revenues from US$443.22 million to US$397.23 million year-over-year, reflecting its unprofitable status. Despite this, the company maintains a strong cash position with short-term assets of US$253.1 million exceeding both short-term liabilities of US$138.2 million and long-term liabilities of US$121.1 million, indicating financial stability in the short term. The debt to equity ratio has improved over five years from 7.3% to 2.2%, but increased volatility and limited cash runway remain concerns for potential investors in penny stocks.

- Click to explore a detailed breakdown of our findings in Caesarstone's financial health report.

- Explore historical data to track Caesarstone's performance over time in our past results report.

Protalix BioTherapeutics (PLX)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: Protalix BioTherapeutics, Inc. is a biopharmaceutical company focused on developing, producing, and commercializing recombinant therapeutic proteins using its ProCellEx plant cell-based protein expression system, with a market cap of $181.29 million.

Operations: The company generates revenue from its Biotechnology (Startups) segment, amounting to $52.74 million.

Market Cap: $181.29M

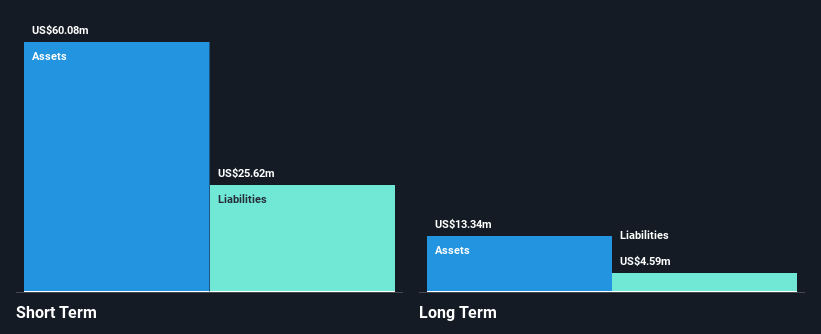

Protalix BioTherapeutics, Inc. has recently secured European Commission approval for a new dosing regimen of pegunigalsidase alfa, potentially enhancing its market position in the treatment of Fabry disease. The approval entitles Protalix to a significant US$25 million regulatory milestone payment from Chiesi Global Rare Diseases. Despite reporting a net loss of US$6.6 million for 2025, the company forecasts increased revenues between US$78 million and US$83 million in 2026, buoyed by expected sales growth and milestone payments. Protalix remains debt-free with short-term assets exceeding liabilities, suggesting financial stability amid its unprofitable status.

- Dive into the specifics of Protalix BioTherapeutics here with our thorough balance sheet health report.

- Explore Protalix BioTherapeutics' analyst forecasts in our growth report.

Next Steps

- Reveal the 361 hidden gems among our US Penny Stocks screener with a single click here.

- Interested In Other Possibilities? The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 20 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com