- On March 30, 2026, JLens and the Anti-Defamation League urged GE Aerospace shareholders to vote against a proposal criticizing the company’s defense business and its product sales to the Israel Defense Forces, arguing it could harm operations and mischaracterizes the role of the U.S. government in foreign military sales.

- The dispute highlights how rising scrutiny of defense supply chains and human rights due diligence is increasingly shaping governance debates around large aerospace contractors like GE.

- With GE Aerospace’s recent earnings beats and raised guidance as a backdrop, we’ll examine how this governance controversy may influence its investment narrative.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 27 best rare earth metal stocks of the very few that mine this essential strategic resource.

General Electric Investment Narrative Recap

To own GE Aerospace, you have to believe its engine and services franchises can keep translating into strong cash generation, even as the business becomes a pure-play aerospace name with more earnings volatility. The JLens and ADL push against the human-rights-focused proposal adds governance noise but does not appear to alter the near term earnings and cash flow trajectory, or the key risk around exposure to commercial aviation cycles.

Against this backdrop, GE’s recent earnings beats and raised guidance, supported by a five year earnings CAGR of 37.1% and a five year free cash flow margin averaging 16.3%, matter more for the stock’s immediate narrative than this governance dispute. They reinforce the core catalyst many shareholders focus on: whether GE can keep converting its large installed base and backlog into growing, high quality cash flows while funding dividends and a US$20,000,000,000 buyback program.

Yet beneath this strength, investors should be aware that concentrated exposure to commercial aviation and ongoing supply chain pressures could still...

Read the full narrative on General Electric (it's free!)

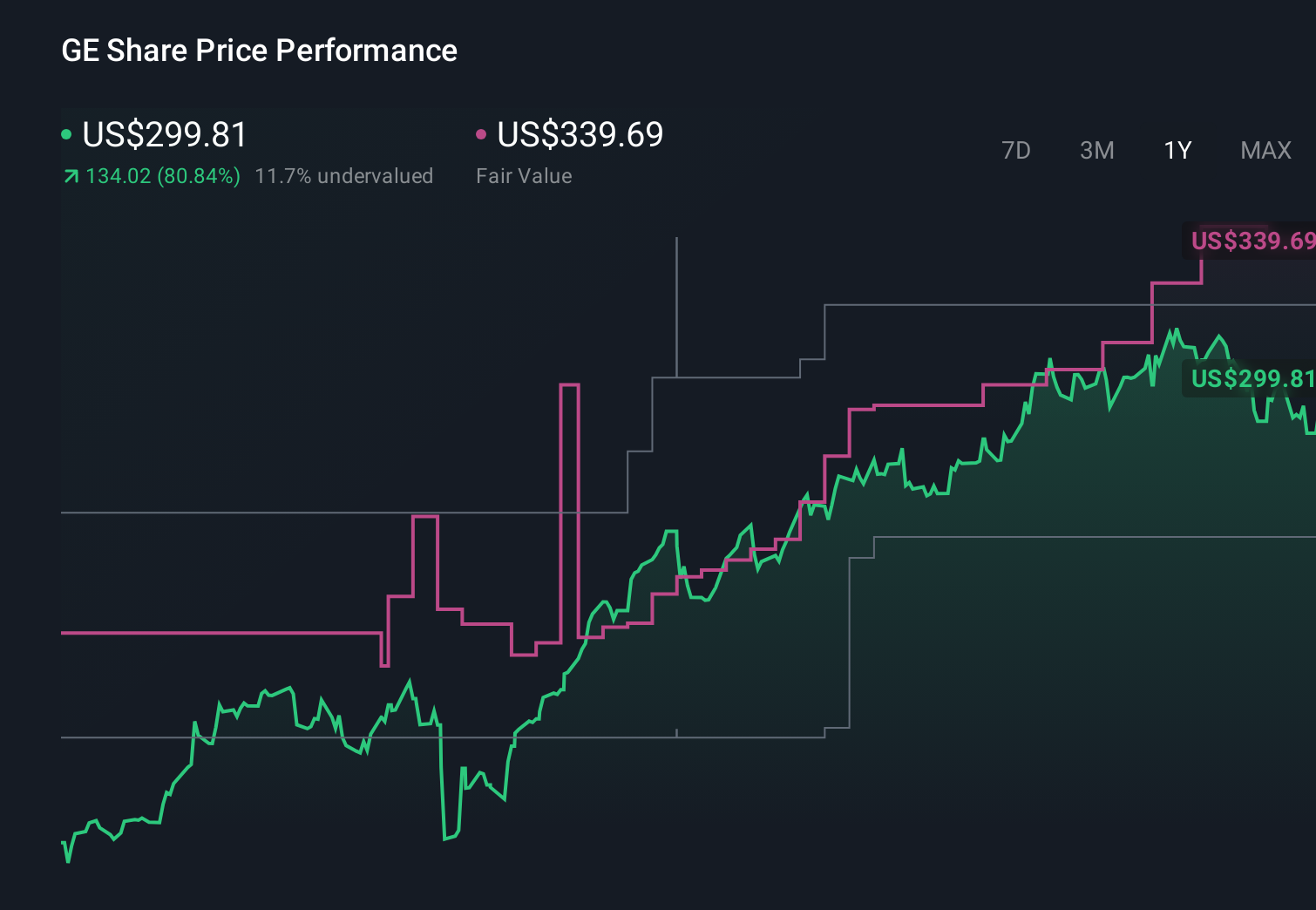

General Electric’s narrative projects $50.8 billion revenue and $9.5 billion earnings by 2028. This requires 6.9% yearly revenue growth and about a $1.9 billion earnings increase from $7.6 billion today.

Uncover how General Electric's forecasts yield a $357.24 fair value, a 14% upside to its current price.

Exploring Other Perspectives

While consensus focuses on solid but moderate growth, the most optimistic analysts were modeling revenue of about US$62,100,000,000 and earnings of US$12,100,000,000 by 2029, which could look very different once governance tensions and geopolitical risk are fully reflected.

Explore 8 other fair value estimates on General Electric - why the stock might be worth 11% less than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your General Electric research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free General Electric research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate General Electric's overall financial health at a glance.

Curious About Other Options?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- AI is about to change healthcare. These 36 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Uncover the next big thing with 32 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com