- Lennox International, a provider of energy-efficient HVAC and refrigeration solutions, recently announced it will report first-quarter 2026 results on April 29, accompanied by a webcast hosted by CEO Alok Maskara and CFO Michael Quenzer.

- Investor enthusiasm has been reinforced by Lennox’s inclusion in a quality investing screen highlighting its financial strength and durable competitive position in the HVAC market, alongside increased interest from technical and AI-driven trading strategies.

- Against this backdrop of heightened anticipation around the upcoming earnings call, we'll explore how Lennox's quality-focused recognition influences its existing investment narrative.

Find 59 companies with promising cash flow potential yet trading below their fair value.

Lennox International Investment Narrative Recap

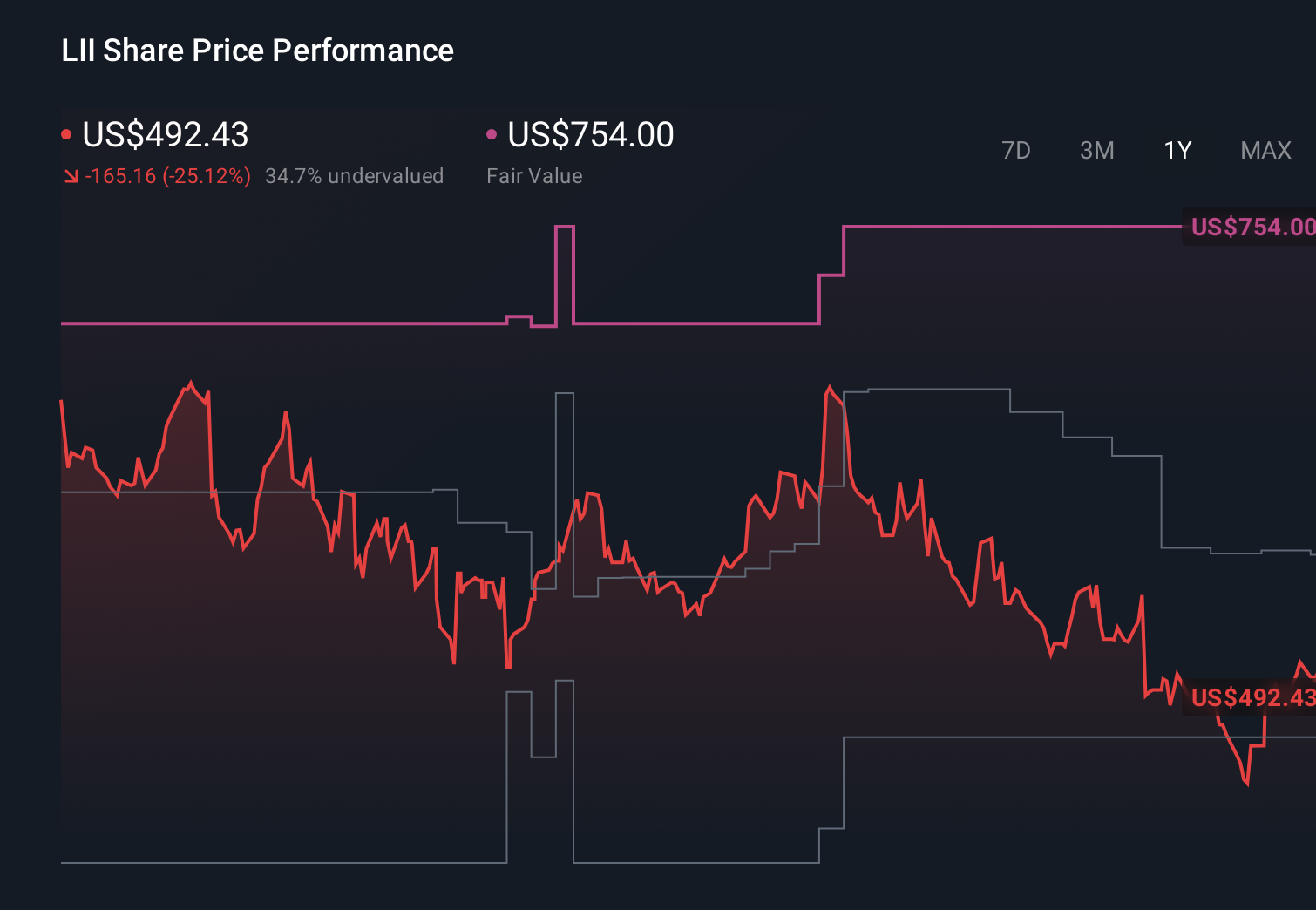

To own Lennox International, you need to believe in long-term demand for energy-efficient HVAC and refrigeration, supported by the company’s strong balance of product innovation and dealer relationships. The key near term catalyst is the upcoming first quarter 2026 earnings call, where management’s comments on volume trends, pricing, and inventories may clarify how resilient margins really are. The latest news about the earnings date and recent share price move does not materially change the primary risk, which remains softer residential demand and elevated cost pressures.

Among recent announcements, Lennox’s inclusion in the Caviar Cruise quality investing screen is particularly relevant here, because it highlights the company’s strong free cash flow, high returns on invested capital, and history of consistent revenue and EBIT growth. Those attributes are central to the bullish narrative that Lennox can sustain pricing power and margin resilience, even as the market worries about housing softness and higher input costs heading into the April 29 earnings update.

Yet beneath the excitement around earnings and quality rankings, investors should also be aware of the risk that prolonged cost inflation and dealer price resistance could eventually squeeze margins and...

Read the full narrative on Lennox International (it's free!)

Lennox International's narrative projects $6.2 billion revenue and $1.1 billion earnings by 2028.

Uncover how Lennox International's forecasts yield a $555.69 fair value, a 10% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts take a much more cautious view, assuming revenue grows only about 2.1% annually and that earnings reach roughly US$1.0 billion by 2028, so this latest burst of AI driven and technical enthusiasm may or may not shift their more conservative expectations.

Explore 2 other fair value estimates on Lennox International - why the stock might be worth as much as 10% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Lennox International research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Lennox International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Lennox International's overall financial health at a glance.

No Opportunity In Lennox International?

Our top stock finds are flying under the radar-for now. Get in early:

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Capitalize on the AI infrastructure supercycle with our selection of the 36 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com