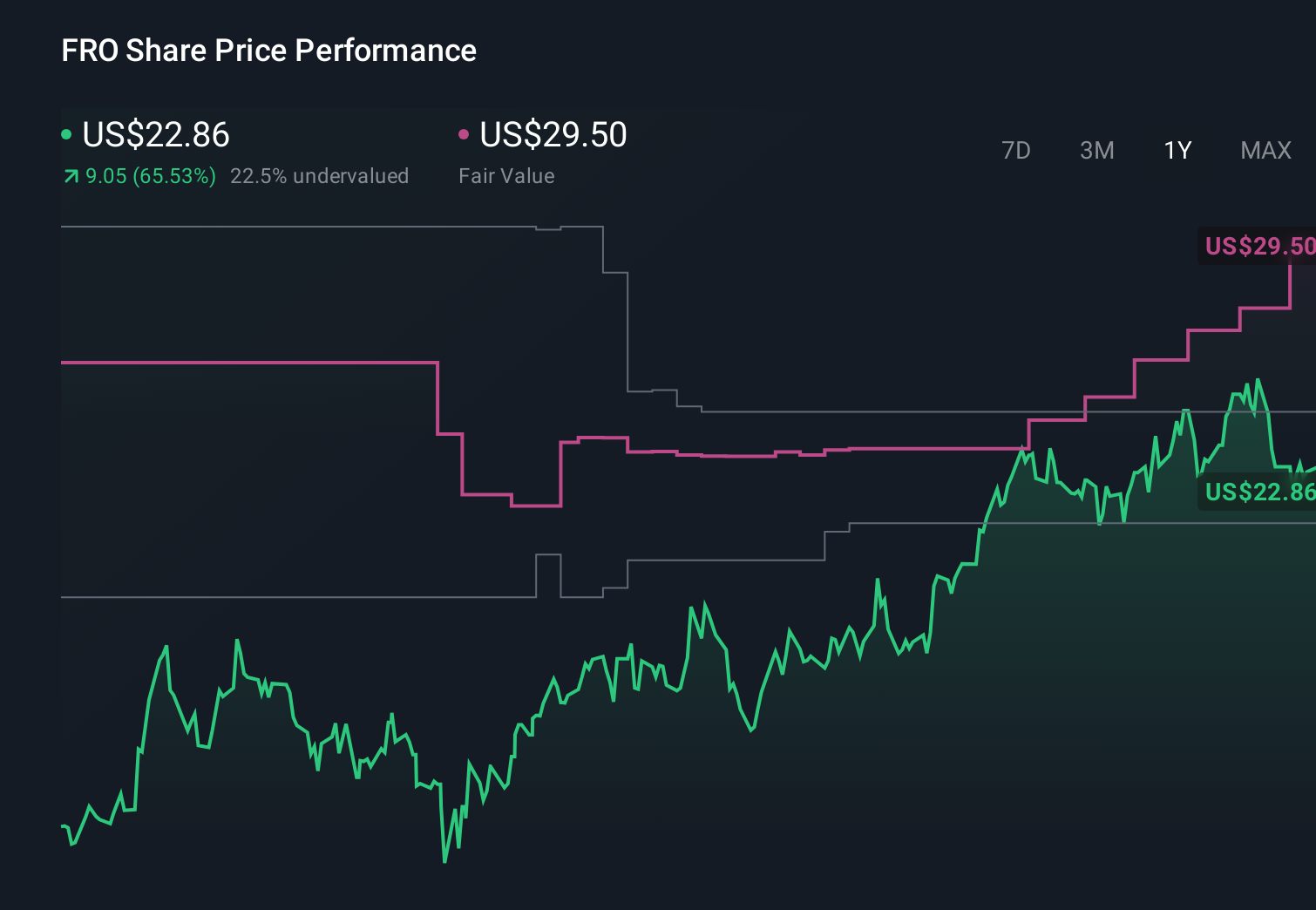

- Earlier this week, Frontline PLC was flagged as trading very far above its estimated intrinsic GF Value, while its financial strength was rated a relatively low 4/10 despite an overall GF Score of 74.

- This mix of perceived overvaluation and balance sheet concerns has sharpened investor focus on whether Frontline’s fundamentals fully underpin its current market optimism.

- Next, we’ll examine how concerns about Frontline’s low financial strength score may reshape its existing investment narrative and risk profile.

Explore 24 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Frontline Investment Narrative Recap

To be a shareholder in Frontline today, you need to believe in the resilience of crude tanker demand and the company’s ability to translate that into cash returns despite industry cyclicality. The recent flag as “significantly overvalued” against GF Value, combined with a 4/10 financial strength score, puts short term attention squarely on balance sheet flexibility as Frontline funds fleet expansion. For now, this news sharpens, rather than materially changes, the key near term catalyst and risk.

The most relevant recent announcement here is the US$1,224.0 million acquisition of nine ECO VLCC newbuildings, to be financed largely through cash and long term debt. This expansion could support earnings power if tanker markets remain supportive, but it also ties directly into the concerns highlighted by the low financial strength rating, as higher leverage and future capital commitments become more central to the risk profile.

Yet behind the strong share price run, investors should be aware of how rising debt commitments could start to affect...

Read the full narrative on Frontline (it's free!)

Frontline's narrative projects $1.6 billion revenue and $697.7 million earnings by 2029. This implies a 7.1% yearly revenue decline but an earnings increase of about $318.6 million from $379.1 million today.

Uncover how Frontline's forecasts yield a $41.25 fair value, a 20% upside to its current price.

Exploring Other Perspectives

The lowest estimate analysts paint a far more cautious picture, assuming revenue falls toward about US$1.6 billion while earnings climb to roughly US$686.0 million, so you should expect that views on balance sheet risk and future cash generation may shift again as this new overvaluation and financial strength signal is digested.

Explore 5 other fair value estimates on Frontline - why the stock might be worth less than half the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Frontline research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Frontline research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Frontline's overall financial health at a glance.

Ready For A Different Approach?

Our top stock finds are flying under the radar-for now. Get in early:

- Find 58 companies with promising cash flow potential yet trading below their fair value.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- We've uncovered the 11 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com