- Investors may be wondering if FirstEnergy at around US$51.43 is offering good value right now, or if the recent optimism has already been priced in.

- The stock has returned 0.2% over the last 7 days, 1.5% over the past month, 13.6% year to date, 31.8% over 1 year, 42.7% over 3 years and 76.7% over 5 years, which puts recent moves into a longer term context.

- Recent coverage around FirstEnergy has focused on its position in the US utilities sector and how the company fits into portfolios looking for regulated electric exposure, as well as general commentary on how income oriented names are being viewed by investors. Together, this context helps explain why the share price has been relatively firm over multiple time frames.

- Despite this share price performance, FirstEnergy currently records a valuation score of 0 out of 6. The discussion ahead will walk through what different valuation methods imply for the stock and then finish with a broader framework that can help readers judge value more confidently over time.

FirstEnergy scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: FirstEnergy Dividend Discount Model (DDM) Analysis

The Dividend Discount Model estimates what a stock could be worth by projecting future dividends and discounting them back to today. It is especially useful when a company is primarily owned for its income stream.

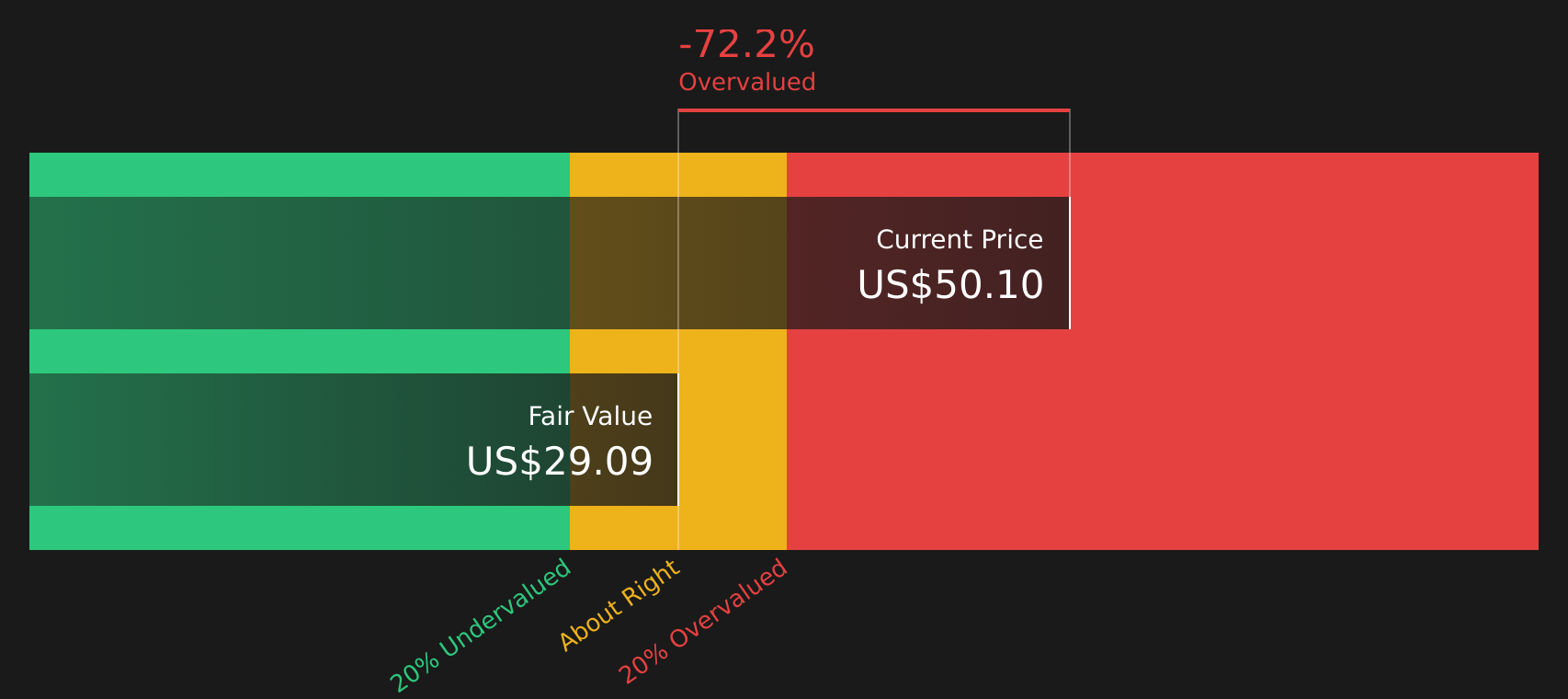

For FirstEnergy, the model uses a dividend per share of about US$2.02, a return on equity of 9.15% and a very high payout ratio of roughly 99.61%. With almost all earnings paid out, the implied long term dividend growth rate is very low at about 0.04%. This is calculated as the small portion of earnings retained multiplied by return on equity.

Based on these inputs, the DDM produces an estimated intrinsic value of about US$29.10 per share. Compared with the recent share price around US$51.43, the model suggests the stock is about 76.7% overvalued. The key point is that, using this dividend-based approach, the current price already more than reflects the income stream that the model assumes.

Result: OVERVALUED

Our Dividend Discount Model (DDM) analysis suggests FirstEnergy may be overvalued by 76.7%. Discover 58 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: FirstEnergy Price vs Earnings

For profitable companies, the P/E ratio is a useful way to think about value because it links what you pay per share directly to the earnings that support that share price.

What counts as a “normal” P/E depends on how quickly earnings are expected to grow and how risky those earnings are. Higher growth or lower perceived risk can justify a higher P/E, while slower growth or higher risk usually point to a lower one.

FirstEnergy currently trades on a P/E of about 29.2x. That sits above the Electric Utilities industry average of about 22.3x and also above the peer group average of roughly 22.9x. On those simple comparisons, the shares look expensive relative to many similar companies.

Simply Wall St’s Fair Ratio, at about 25.2x, goes a step further. It is a proprietary estimate of what a “reasonable” P/E might be after accounting for factors such as earnings growth characteristics, profit margins, industry, market cap and company specific risks. Because it blends these elements, it can offer a more tailored reference point than a basic industry or peer comparison.

Compared with this Fair Ratio, FirstEnergy’s current P/E of 29.2x is higher, which points to the shares trading on a richer multiple than that model would suggest.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Upgrade Your Decision Making: Choose your FirstEnergy Narrative

Earlier it was mentioned that there is an even better way to think about valuation. Meet Narratives, a simple way to describe your story for FirstEnergy, link that story to a forecast for revenue, earnings and margins, and then see a fair value that you can compare with the current price on Simply Wall St’s Community page. Narratives are updated automatically when fresh news or earnings arrive. One investor might see FirstEnergy as worth around the analysts’ US$52.46 fair value based on steady revenue growth and margin assumptions, while another might plug in more cautious expectations around legal or capital spending risks and arrive at a lower fair value. This can help each of them decide whether the current price near US$51.43 looks high, low or roughly in line with their own view.

Do you think there's more to the story for FirstEnergy? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com