SFL Corporation (NYSE:SFL) heads into its 2026 Annual General Meeting on May 11 with a proposal to convert 25 million authorized but unissued common shares into preference shares, directly affecting how future capital raising could look.

See our latest analysis for SFL.

At a share price of $10.84, SFL has seen momentum build recently, with a 30-day share price return of 2.65% and a 90-day share price return of 30.60%. The 1-year total shareholder return of 55.08% reflects stronger long-term gains.

If this kind of capital structure rethink has your attention, it can be useful to see what else is moving in related areas of the market via our 30 power grid technology and infrastructure stocks

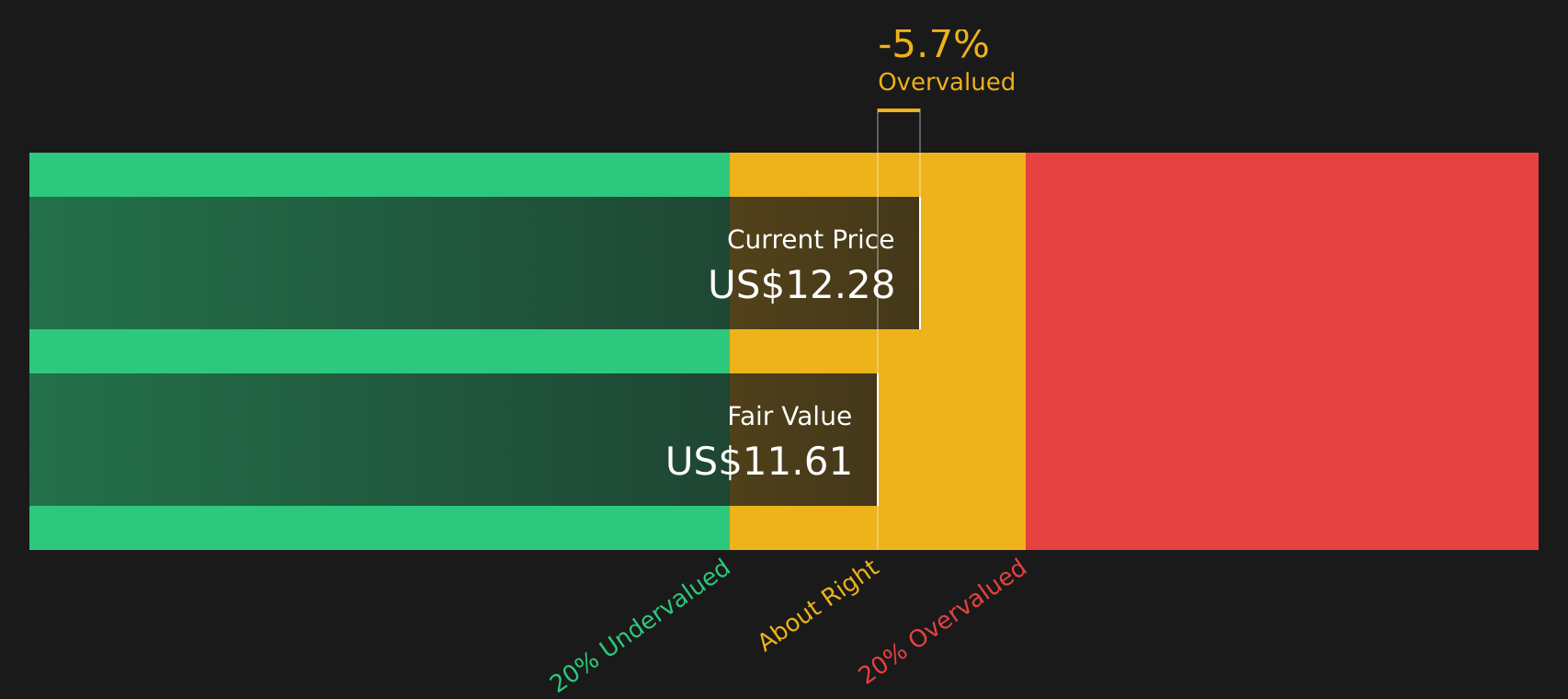

With SFL trading at $10.84, close to an analyst price target of $10.55 and a modest 2.1% intrinsic discount, the key question is whether there is still upside potential available or whether the market is already fully pricing in future growth.

Most Popular Narrative: 15% Overvalued

Against the last close of $10.84, the most followed narrative points to a fair value of $9.43, framing SFL as modestly ahead of its modeled cash flows.

With $4.2 billion in charter backlog (two-thirds with investment-grade customers) and available liquidity exceeding $300 million, SFL is positioned to capitalize on increased global trade and supply chain resilience initiatives, potentially enabling accretive asset growth and supporting future revenue expansion.

Want to see what sits behind that backlog story? The narrative leans on revenue forecasts, margin shifts and a future profit multiple that needs everything to line up.

The fair value view here uses a 9.28% discount rate to bring projected cash flows back to today, so the gap to the $10.84 share price reflects those long term assumptions about earnings power, capital returns and the contract book, rather than short term price momentum.

Result: Fair Value of $9.43 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that story can quickly change if container demand softens or if the Hercules rig stays idle for longer, putting pressure on cash flow and contract coverage.

Find out about the key risks to this SFL narrative.

Another Way To Look At Value

The most popular narrative frames SFL as about 15% overvalued at $10.84 versus a $9.43 fair value. In contrast, the SWS DCF model points the other way, with fair value at $11.07 and the shares trading at a 2.1% discount. Which story do you think best fits the cash flows you expect?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

With mixed signals on value and sentiment, the real question is how this all lines up for you right now. Move quickly, review the full picture, and weigh both the potential upsides and the areas of concern via the 2 key rewards and 2 important warning signs.

Looking for more investment ideas?

If SFL is on your radar, do not stop there. Broaden your watchlist with other focused ideas so you are not the one hearing about them last.

- Target stability with companies that prioritise resilience and consistent fundamentals through the 72 resilient stocks with low risk scores.

- Hunt for quality at a discount by scanning companies that appear attractively priced using the 58 high quality undervalued stocks.

- Zero in on stocks that pair solid financial footing with cleaner balance sheets via the solid balance sheet and fundamentals stocks screener (41 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com