- Earlier this month, Inspectorio announced that Gap Inc. will deploy its AI-powered platform across the global supply chains of Old Navy, Gap, Banana Republic, and Athleta to automate tasks, deepen product traceability, and strengthen quality and sustainability oversight.

- This move could reshape how Gap manages risk and transparency across thousands of suppliers, potentially redefining operational standards in mass-market apparel.

- Next, we'll examine how this AI-driven supply chain upgrade could influence Gap's investment narrative around efficiency, margins, and resilience.

Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

Gap Investment Narrative Recap

To own Gap today, you need to believe its brand refresh, disciplined cost control, and capital returns can offset tariff pressure, competitive threats, and patchy category execution. The Inspectorio partnership fits neatly into the existing catalyst of tech-led supply chain improvement, but on its own it does not materially shift the key near term driver (execution on core brands) or the main risk (margin pressure from costs and discounting).

Against this backdrop, the recent US$1.0 billion share buyback authorization stands out. It highlights management’s confidence in Gap’s cash generation and provides support as the company invests in AI tools like Inspectorio to tighten inventory, improve quality oversight, and potentially protect margins if demand softens or promotions rise.

But while AI may help with efficiency, investors still need to be aware that...

Read the full narrative on Gap (it's free!)

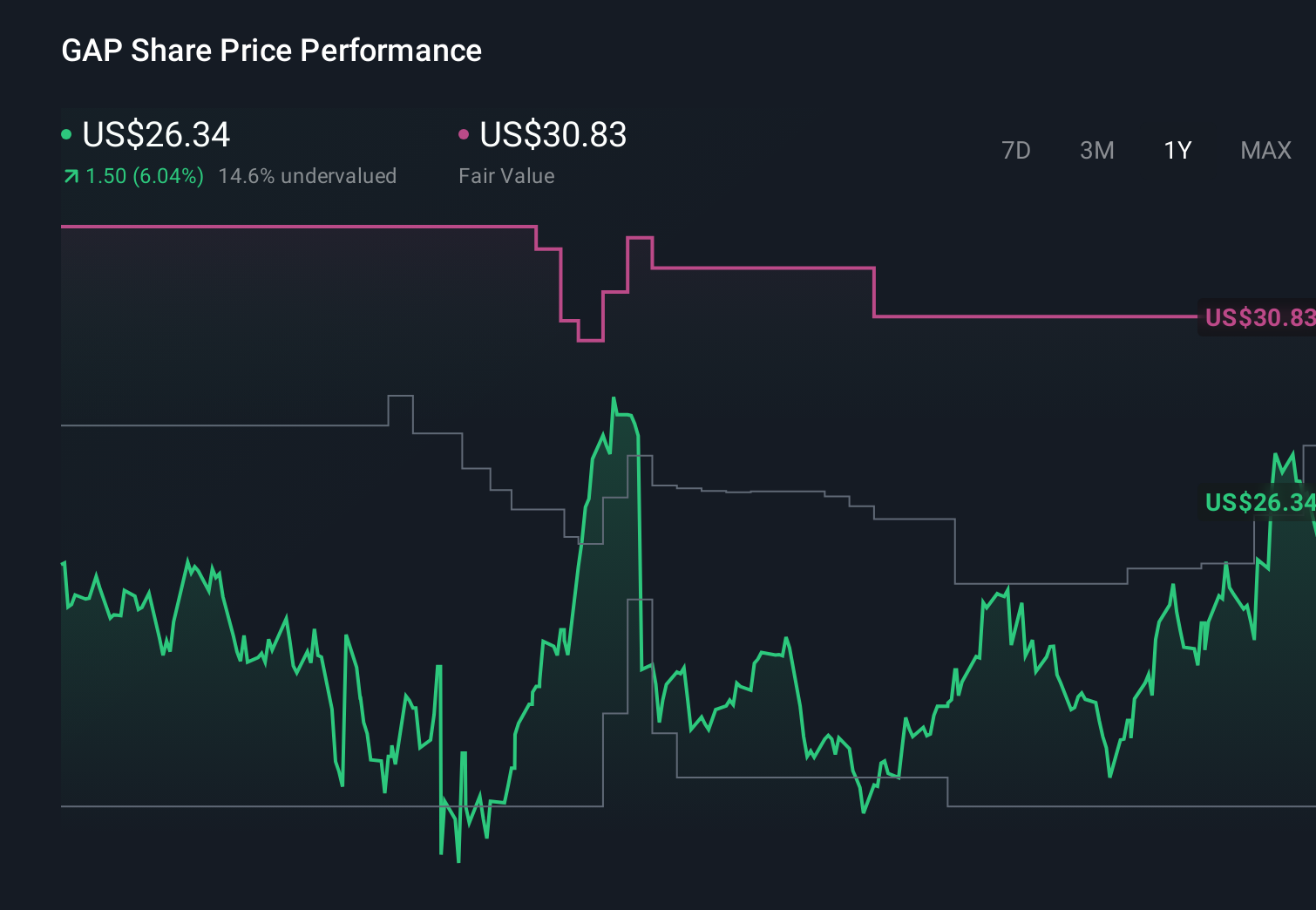

Gap’s narrative projects $16.6 billion revenue and $1.0 billion earnings by 2029.

Uncover how Gap's forecasts yield a $30.65 fair value, a 17% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were assuming revenue would creep to about US$15.6 billion and earnings to roughly US$820 million, and they worry that even investments in AI driven supply chain tools might not fully offset risks from rising costs and online competition, so it is worth weighing their more cautious view against the more optimistic case around technology and brand progress.

Explore 9 other fair value estimates on Gap - why the stock might be worth as much as 47% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Gap research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Gap research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Gap's overall financial health at a glance.

Want Some Alternatives?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 21 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 27 best rare earth metal stocks of the very few that mine this essential strategic resource.

- We've uncovered the 11 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com