Klarna Group (KLAR) is back in focus after expanding its partnership with premium beauty retailer DOUGLAS Group to Italy and Spain, bringing its flexible, interest free installment payment options to more Southern European shoppers.

See our latest analysis for Klarna Group.

Despite the DOUGLAS expansion and other recent partner wins such as B-Parts, sentiment around Klarna Group has been weak. The 30 day share price return shows a 20.63% decline and the year to date share price return shows a 54.36% decline from the current US$13.04 level. This suggests investors are still reassessing growth potential and risk.

If Klarna’s latest moves in payments have your attention, this could be a good moment to widen your search and check out 18 top founder-led companies

With revenue of US$3,509 million, an annual net loss of US$294 million and a share price that has fallen sharply to US$13.04, is Klarna Group being marked down too far, or are markets already pricing in expectations of future growth?

Most Popular Narrative: 69.7% Undervalued

According to the most followed narrative, Klarna Group’s fair value sits at $43.01 per share, a long way from the last close at $13.04, and that gap is what drives the valuation story.

My fair value of $43.01 represents a significant vote of confidence in Klarna’s ability to maintain this trajectory. While the broader market often fluctuates based on interest rate fears, the "narrative of the $43" is one of undervalued efficiency.

Curious what supports that $43.01 figure? The narrative leans heavily on sustained revenue expansion, rising profitability and a future earnings multiple that assumes Klarna matures into a full scale digital bank. The exact growth, margin and valuation assumptions are all laid out in the full story.

Result: Fair Value of $43.01 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this story can break if credit losses weigh on that US$294 million net loss or if revenue growth of 16.51% slows meaningfully.

Find out about the key risks to this Klarna Group narrative.

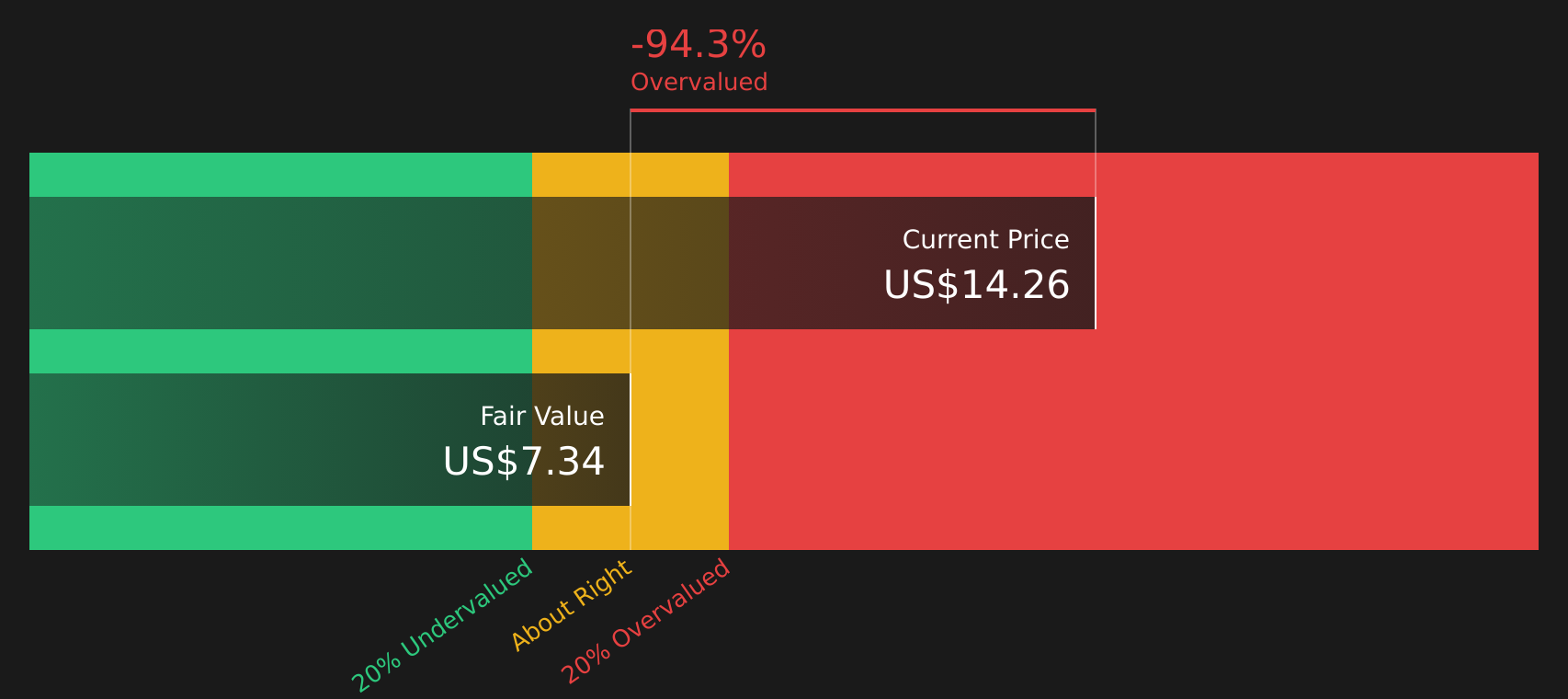

Another View: DCF Puts Klarna On The Other Side Of Fair Value

There is a clear tension between the $43.01 narrative fair value and our DCF model. While the narrative points to undervaluation, the SWS DCF model suggests the opposite, with Klarna trading at $13.04 compared with an estimated future cash flow value of $7.28, which screens as overvalued on that basis.

For you as an investor, that gap highlights two very different stories: one built on revenue growth and future banking ambitions, and the other grounded in projected cash flows. Which story feels more robust for your own thesis: the growth path or the cash flow math?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Klarna Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 58 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment clearly split between growth optimism and cash flow caution, this is a good time to look at the data yourself and decide where you stand. You can start with 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Klarna has sharpened your interest, do not stop here. Broadening your watchlist with other well defined opportunities can help you build a more resilient portfolio.

- Spot potential turnarounds by scanning 33 elite penny stocks with strong financials that pair small size with comparatively stronger financial profiles.

- Strengthen your core holdings by reviewing 58 high quality undervalued stocks that combine solid cash flows with quality balance sheets.

- Dial down portfolio stress by considering 72 resilient stocks with low risk scores that screen well on risk metrics and business resilience.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com