- In early April 2026, Salesforce filed a shelf registration for US$41.18 million of common stock linked to its employee stock ownership plan, while partners such as Solutions by Text and Redpanda expanded integrations that deepen Salesforce’s role at the center of compliant messaging and data streaming workflows.

- At the same time, investors are wrestling with whether Salesforce’s AI initiatives, like Agentforce and Slackbot, will offset competitive, pricing, and workflow-disruption risks that are prompting some institutions to exit the stock even as others highlight strong AI adoption and a solid balance sheet.

- Next, we’ll examine how AI disruption fears, alongside accelerating Agentforce and Slackbot adoption, could reshape Salesforce’s investment narrative for long-term investors.

Find 58 companies with promising cash flow potential yet trading below their fair value.

Salesforce Investment Narrative Recap

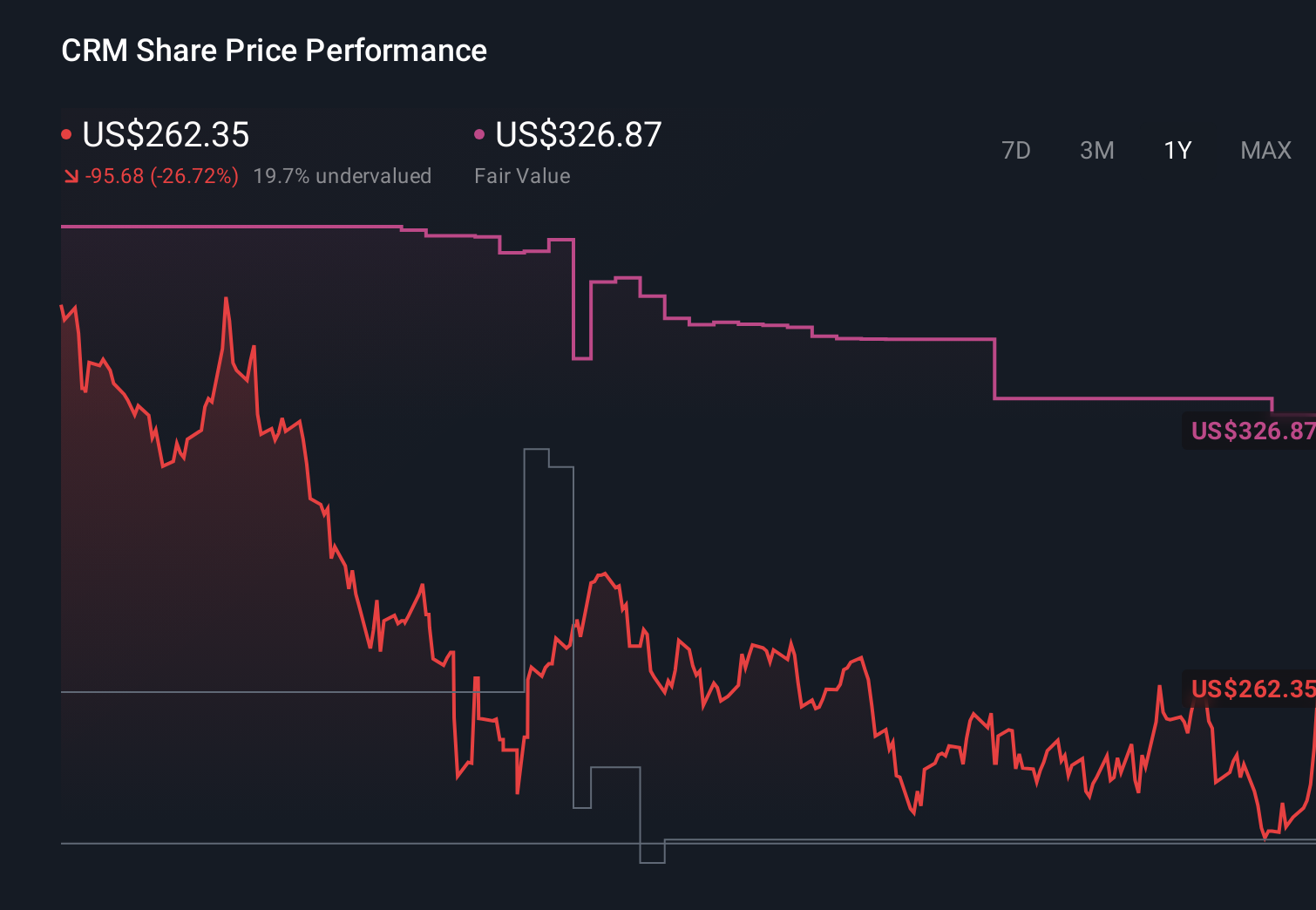

To own Salesforce today, you need to believe its push into AI agents and Data Cloud can offset competitive pressure, pricing shifts, and workflow disruption risk. The recent ESOP related shelf registration is not material to that thesis, but the market’s focus has zeroed in on whether Agentforce and Slackbot adoption can remain a key short term catalyst while AI agents potentially compress traditional seat based CRM revenues.

The freshest integration news that matters here is Solutions by Text plugging compliant SMS, MMS, and RCS directly into Salesforce Marketing Cloud. It reinforces Salesforce’s role as a workflow and compliance hub for regulated industries, which matters if you think AI driven automation will deepen rather than replace CRM centric journeys and help support Data Cloud and Agentforce usage growth over time.

Yet, even as AI momentum builds, investors should not ignore the risk that aggressive AI automation could eventually reduce software seat counts and recurring license demand...

Read the full narrative on Salesforce (it's free!)

Salesforce's narrative projects $51.9 billion revenue and $10.3 billion earnings by 2028. This requires 9.6% yearly revenue growth and a roughly $3.6 billion earnings increase from $6.7 billion today.

Uncover how Salesforce's forecasts yield a $317.21 fair value, a 92% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were penciling in about US$56.2 billion of revenue and US$12.0 billion of earnings by 2028, yet this latest AI driven volatility and automation risk reminder show how quickly those upbeat scenarios might be reassessed, so it is worth weighing both the bullish lock in story and the possibility that AI agents could blunt Salesforce’s traditional growth engines.

Explore 37 other fair value estimates on Salesforce - why the stock might be worth over 2x more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Salesforce research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Salesforce research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Salesforce's overall financial health at a glance.

Looking For Alternative Opportunities?

Our top stock finds are flying under the radar-for now. Get in early:

- Capitalize on the AI infrastructure supercycle with our selection of the 36 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Explore 24 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Rare earth metals are the new gold rush. Find out which 27 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com