StoneX Group (SNEX) recently announced a partnership with The Pathfinder Group to plug its global payments infrastructure into Pathfinder’s WITS wire platform, giving more financial institutions access to institutional-grade cross-border payments.

See our latest analysis for StoneX Group.

The partnership news comes after a strong run in the shares, with a 34.6% 30 day share price return and a 43.1% year to date share price return, while the 5 year total shareholder return of 375.1% points to sustained compounding.

If this kind of payments focused story has your attention, it could be a good moment to widen your search with our screener of 18 top founder-led companies

With StoneX shares now around US$92.90, very close to the latest analyst target of US$92.00 and carrying a low value score of 1, the key question is whether the recent rally leaves any mispricing or if the market is already accounting for future growth.

Price to Earnings of 21x: Is it justified?

On a P/E of 21x, with the last close at $92.90, StoneX trades above its estimated fair P/E of 13.8x and above the peer average of 16x, while still below the wider US Capital Markets industry average of 39.1x.

The P/E ratio links the share price to earnings, so a higher multiple typically reflects higher expectations for future profit growth or perceived quality of those earnings. For a diversified financial services group like StoneX, which spans commercial hedging, institutional trading, retail platforms and payments, the P/E becomes a shorthand for how the market is weighing that earnings mix and its durability.

Here, the market is assigning a richer P/E than the peer average, which suggests investors are willing to pay more for each dollar of StoneX earnings than for similar companies. However, the current 21x multiple sits above the estimated fair P/E of 13.8x. This level points to a lower price that the market could reference if expectations were to cool, even though it still stands at a discount to the broader industry multiple of 39.1x.

Explore the SWS fair ratio for StoneX Group

Result: Price-to-Earnings of 21x (OVERVALUED).

However, the premium P/E leaves little room for disappointment if net income growth of 10.2% slows or if analyst expectations around the US$92.00 target shift.

Find out about the key risks to this StoneX Group narrative.

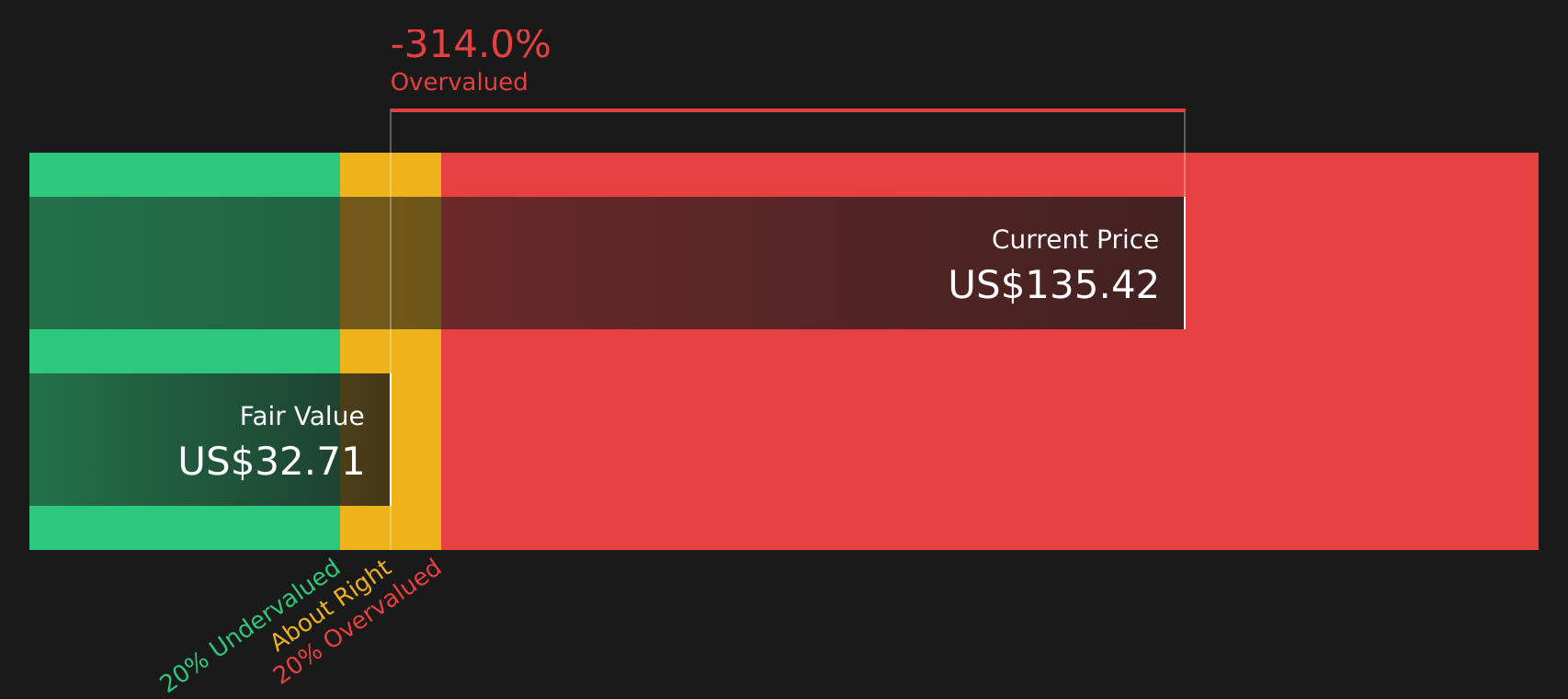

Another View: Cash Flows Paint A Sharper Picture

While the 21x P/E points to an expensive share price relative to the fair ratio of 13.8x and peers at 16x, our DCF model goes further and suggests StoneX at $92.90 is trading well above an estimated future cash flow value of $29.44, raising a different set of questions about valuation risk.

For a closer look at how this cash flow view is built and where assumptions matter most, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out StoneX Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 58 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mixed signals in this story have you weighing the upside against the valuation risk, it can help to act quickly and test the numbers yourself. To understand why some investors remain optimistic, review the 3 key rewards

Looking for more investment ideas?

If StoneX has sharpened your focus on valuation and quality, do not stop here. Widen your search now so you are not late to the next idea.

- Target companies that trade below what their quality might suggest by starting with 58 high quality undervalued stocks.

- Prioritize financial strength and resilience by checking companies in the solid balance sheet and fundamentals stocks screener (41 results).

- Spot potential opportunities that others may be overlooking by reviewing our screener containing 23 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com