Context for Coterra Energy’s recent share performance

Coterra Energy (CTRA) has drawn attention after recent share moves, including a 1 day return of around a 1.2% decline and a 4.8% decline over the past week, alongside stronger gains over the past month and the past 3 months.

See our latest analysis for Coterra Energy.

Zooming out, the recent share price pullback sits against a stronger backdrop, with a 24.1% year to date share price return and a 35.37% 1 year total shareholder return that suggest momentum has been building.

If you are looking for more ideas in the energy space, this could be a good moment to see what other producers are doing through our 93 nuclear energy infrastructure stocks

With Coterra earning a top value score of 5, trading at $33.01 against an average analyst target of $37.59, and showing an implied intrinsic discount of about 66%, is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 29.2% Overvalued

According to Bejgal, the narrative fair value of $25.55 sits below Coterra Energy’s last close at $33.01, which sets up a more cautious valuation stance.

In 3 years, Coterra is likely to solidify its position as a leading energy producer with enhanced capital efficiency and diversified revenue streams. By 5 years, the company could see robust earnings growth driven by the LNG market and efficient oil production. Over 10 years, its extensive inventory and focus on innovation position it for sustainable long-term growth.

Want to see what is behind this confident long term earnings view? The narrative leans heavily on LNG driven revenue, rising margins and a richer future earnings multiple.

Result: Fair Value of $25.55 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this story can change quickly if LNG demand or pricing weakens, or if new environmental rules in key regions raise costs and pressure returns.

Find out about the key risks to this Coterra Energy narrative.

Another view on Coterra’s value

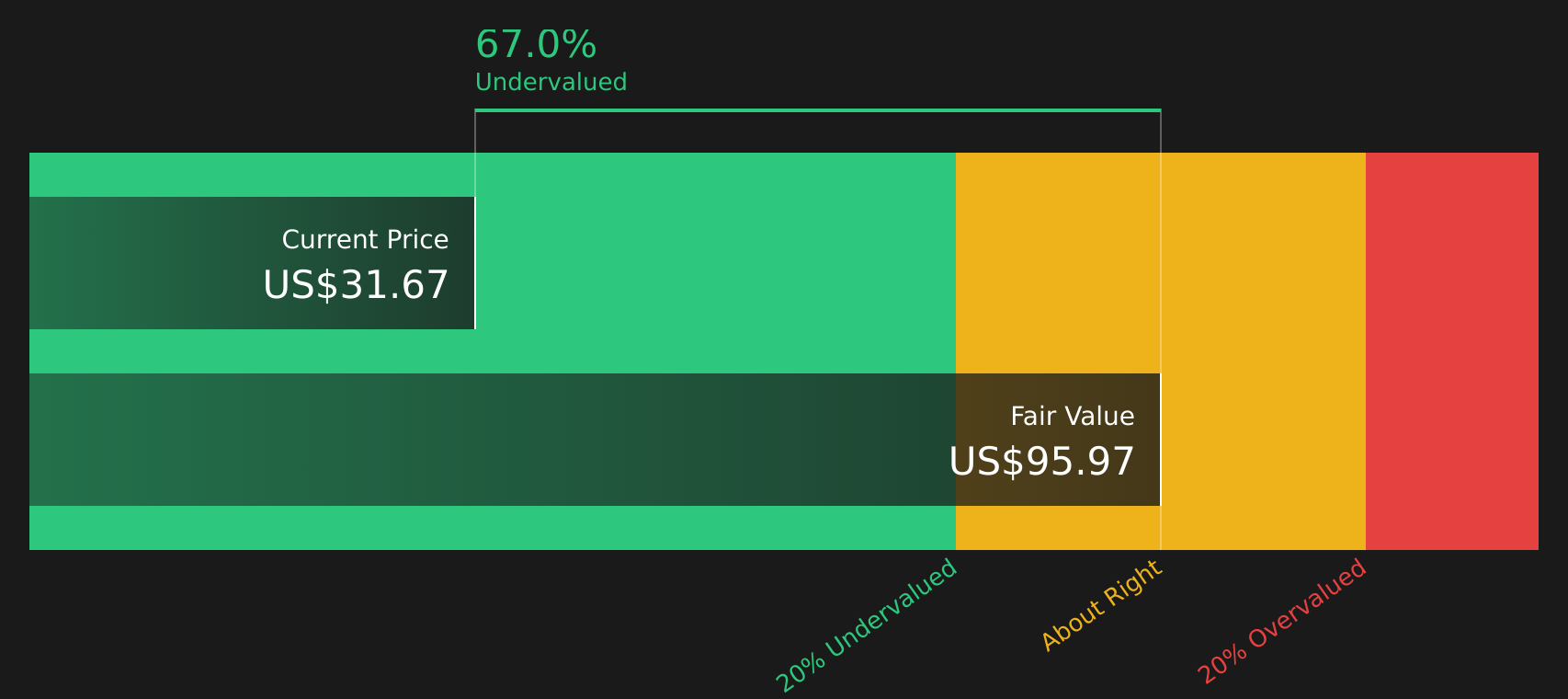

The user narrative sees Coterra as 29.2% overvalued at $33.01 versus a fair value of $25.55, yet our DCF model points the other way, with an estimated future cash flow value of $95.97, or around 65.6% above the current price. When two grounded methods disagree this much, which one do you put more weight on?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

The split between risks and rewards in this story is clear, so move fast, review the underlying numbers yourself and weigh up the 4 key rewards and 1 important warning sign

Looking for more investment ideas?

If Coterra has caught your eye, do not stop here. Use this moment to line up a few more potential opportunities before the market moves on.

- Target potential mispricings by scanning 55 high quality undervalued stocks that combine solid fundamentals with room for a stronger market view.

- Strengthen your income watchlist by checking out 10 dividend fortresses built around higher yielding companies with substantial payouts.

- Reduce portfolio stress by focusing on 73 resilient stocks with low risk scores that score well on resilience and financial robustness.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com